How specialty financing can help investors ride out Japan’s stock market volatility

17 September 2024

The recent bout of volatility in global equity markets is a reminder of the benefits of a long-term view of an investment portfolio. Securities-based financing can help investors who don’t want to be caught out by similar short-term moves in the future.

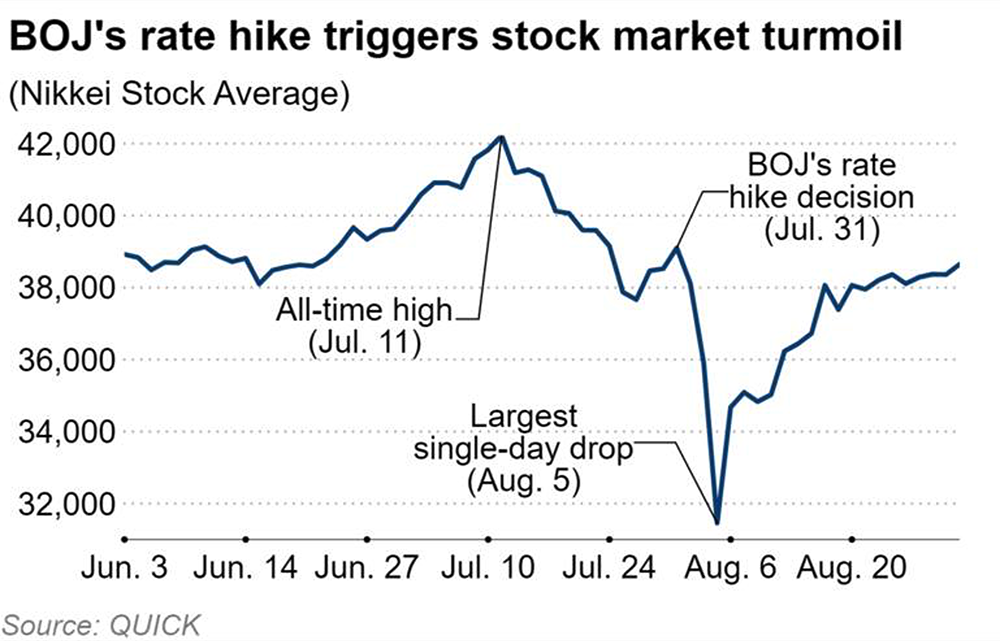

On August 5th, 2024, Japan’s benchmark Nikkei 225 stock index suffered its largest single-session drop since the global market crash of 1987 known as “Black Monday.” But the next day, the index recorded its largest single-day gain since 2008, and proceeded to inch higher into September. This recent volatility appears to have resulted in a shake-out of short-term and speculative investors, while those with a long-term horizon appear intent on standing firm, observed Yue Bamba, Blackrock’s Head of Active Investments for Japan, in an interview with Nikkei Asia.[1]

Figure: The Bank of Japan’s rate hike had a short, sharp impact on stocks

The Nikkei’s plunge in August resulted from a rapid unwinding of the largest “carry trade” the world has ever seen. In a carry trade, an investor borrows in a currency with low interest rates and reinvests the proceeds in higher-yielding assets elsewhere. In this case, investors were borrowing in yen and investing in assets in other currencies, such as US tech stocks.

After the Bank of Japan surprised observers by raising interest rates in July to levels unseen in 15 years,[2] alongside the increasing prospect of imminent rate cuts by the US Federal Reserve,[3] the yen has strengthened sharply, narrowing the arbitrage potential of the yen carry trade. This prompted speculators who financed their trades with borrowed yen to dump their positions, driving down stock prices globally. In Japan, concerns that a stronger yen would hurt exports also hit local stocks.

The decline was exacerbated because many retail investors who had bought equities on margin – which accounts for about 70% of retail trading value in Japan[4] — were forced to sell as prices plunged. Margin trading shrank considerably in the aftermath of Japan’s stock market turmoil.[5]

But while short-term and margin-dependent investors were exiting the Japanese market, domestic institutional investors took the opportunity to snap up 794.2 billion yen (US$5.5 billion) of local stocks at a bargain in the week ending August 9th, according to Tokyo Stock Exchange data.[6] Foreign investors also saw an opportunity, making net purchases of 495.4 billion yen of Japanese stocks that week, while retail investors were net sellers.

Steadfast in their convictions

Several analysts noted in the wake of the August 5th crash that Japan’s long-term underlying fundamentals remain sound. While the strengthening yen could hurt exporters’ profits, the central bank’s move to raise interest rates also signals its confidence in the economy,[7] which, in turn, bodes well for domestically focused businesses. Banks could also benefit from higher rates.

"We continue to believe improvement of domestic economy is a key catalyst for Japanese equities to move higher, and we remain constructive over the medium term,” said Kazunori Tatebe, a strategist at Goldman Sachs.[8]

More broadly, the new wave of investor optimism about Japan appears to be largely intact, at least for those with long-term horizons. Among others, analysts at Citi have maintained their bullish long-term outlook on the back of improved “micro and macro” fundamentals.[9] These include resilient corporate earnings despite volatility in foreign exchange markets, a lower appreciation of the yen than initially expected, a growing number of companies announcing or increasing share buybacks and signs of improved private consumption.

Morgan Stanley described the recent market chaos as an opportunity to buy Japanese stocks at attractive valuations. It sees long-term potential from four key structural changes underway in Japan:[10]

The economic recovery, which is bolstering employment, consumption and capital spending. A relatively weak yen is also supporting exporters.

Companies adopting investor-friendly reforms, including increased rights for minority shareholders.

Companies returning more capital to shareholders through higher dividends and a steep expansion of share buybacks.

The government’s introduction of incentives for locals to buy stocks, including a program to offer tax exemptions for small investments.

Guarding against future shocks

Japanese stocks had clawed back much of their losses by September, and several fund managers see room for further gains as overseas buyers continue to return.[11] BlackRock’s Bamba, for example, sees upside given that many global long-term investors are still underweight on the market, which could change once they have carried out their due diligence.[12]

Also brightening the outlook for Japanese stocks, Bank of Japan officials appeared to downplay the prospects of further imminent interest rate rises while markets remain volatile.[13]

Nevertheless, the recent performance of Japanese equities, and those elsewhere, is a reminder that valuations of long-term shareholdings can change on a dime. This volatility is especially troubling for shareholders whose wealth is highly concentrated in one or a handful of stocks.

Long-term shareholders can insulate themselves from periods of heightened volatility by using securities-backed financing to raise capital without having to sacrifice upside potential. In turbulent times like these, specialty financing provides investors a convenient way to manage their portfolios.

Past performance does not guarantee future returns, and individual returns are not guaranteed or warranted.

This Document is intended solely for accredited investors, sophisticated investors, professional investors, or otherwise qualified investors, as may be required by law or otherwise, and it is not intended for, and should not be used by, persons who do not meet the relevant requirements. The content provided herein is for informational purposes only and is general in nature and not targeted to any specific objective or financial need. The views and opinions expressed in this Document have been prepared by third parties and do not necessarily reflect the views and opinions of EquitiesFirst. EquitiesFirst has not independently examined or verified the information provided herein, and no representation is made that it is accurate or complete. Opinions and information herein are subject to change without notice. The content provided does not constitute an offer to sell (or solicitation of an offer to purchase) any securities, investments, or any financial products (“Offer”). Any such Offer shall only be made through a relevant offering or other documentation which sets forth its material terms and conditions. Nothing contained in this Document shall constitute a recommendation, solicitation, invitation, inducement, promotion, or offer for the purchase or sale of any investment product by Equities First Holdings, LLC or its subsidiaries (collectively, “EquitiesFirst”), nor shall this Document be construed in any way as investment, legal, or tax advice, or as a recommendation, reference, or endorsement by EquitiesFirst. You should seek independent financial advice prior to making an investment decision about a financial product.

This Document contains the intellectual property of EquitiesFirst in the United States and other countries, including, without limitation, their respective logos and other registered and unregistered trademarks and service marks. EquitiesFirst reserves all rights in and to their intellectual property contained in this Document. The Document should not be distributed, published, reproduced or otherwise made available in whole or in part by recipients to any other person and, in particular, should not be distributed to persons in any country where such distribution may lead to a breach of any legal or regulatory requirement.

EquitiesFirst make no representation or warranty with respect to this Document and expressly disclaim any implied warranty under law. You acknowledge that EquitiesFirst is not liable under any circumstances for any direct, indirect, special, consequential, incidental, or punitive damages whatsoever, including, without limitation, any lost profits or lost opportunity, even if EquitiesFirst has been advised of the possibility of such damages.

EquitiesFirst makes the following further statements that may be applicable in the stated jurisdiction:

Australia: Equities First Holdings (Australia) Pty Ltd (ACN: 142 644 399) holds an Australian Financial Services Licence (AFSL Number: 387079). All rights reserved.

The information contained on this Document is intended for persons located in Australia only and classified as a Wholesale Client only as defined in Section 761G of the Corporations Act 2001. The distribution of information to persons outside this criteria may be restricted by law and persons who come into possession of it should seek advice and observe any such restriction.

The material contained in this Document is for information purposes only and should not be construed as an offer or solicitation or recommendation to buy or sell financial products.

The information contained in this Document is intended to be general in nature and is not personal financial product advice. Any advice contained in the Document is general advice only and has been prepared without considering your objectives, financial situation or needs. Before acting on any information, you should consider the appropriateness of the information provided and the nature of the relevant financial product having regard to your objectives, financial situation and needs. You should seek independent financial advice and read the relevant disclosure statements or other offer documents prior to making an investment decision about a financial product.

Forecasts are not guaranteed, and undue reliance should not be placed on them. This information is based on views held by Equities First Holdings (Australia) Pty Ltd as at the publishing date of this material.

Dubai: Equities First Holdings Hong Kong Ltd (DIFC Representative Office) at Gate Precinct Building 4, 6th Floor, Office 7, Dubai International Financial Centre (commercial license number CL7354) is regulated by the Dubai Financial Services Authority (“DFSA”) as a Representative Office (DFSA Firm Reference No.: F008752). All rights reserved.

The information contained in this document is intended to be general in nature, and, to the extent that it is perceived as advice, any advice contained in this document is general advice only and has been prepared without considering your objectives, financial situation, suitability of the financial products or your needs.

The material contained in this document is for information purposes only and should not be construed as financial advice, including an offer or solicitation or recommendation to buy or sell financial products. The information contained in this document is intended to be general in nature and any advice contained in this document is general advice only and has been prepared without considering your objectives, financial situation, suitability of the financial products or your needs. Before acting on any information, you should consider the appropriateness of the information provided and the nature of the relevant financial product having regard to your objectives, financial situation and needs. If you do not understand the contents of this document, you should consult an authorised financial adviser.

This document relates to a financial product which is not subject to any form of regulation or approval by the DFSA. The DFSA has no responsibility for reviewing or verifying any documents in connection with this financial product. Accordingly, the DFSA has not approved this document or any other associated documents nor taken any steps to verify the information set out in this document, and has no responsibility for it.

Hong Kong: Equities First Holdings Hong Kong Limited is licensed under the Money Lenders Ordinance (Money Lender’s Licence No. 1659/2024) and to carry on the business of dealing in securities (Type 1 licence) under the Securities and Futures Ordinance (“SFO”) (CE No. BFJ407). This Document has not been reviewed by the Hong Kong Securities and Futures Commission. It is not intended as an offer to sell securities or a solicitation to buy any product managed or provided by Equities First Holdings Hong Kong Limited and is only intended for persons who qualify as Professional Investors under the SFO. This document is not directed to individuals or organizations for whom such offers or invitations would be unlawful or prohibited.

Korea: The foregoing is intended solely for sophisticated investors, professional investors or otherwise qualified investors who have sufficient knowledge and experience in entering into securities financing transactions. It is not intended for, and should not be used by, persons who do not meet those criteria.

United Kingdom: Equities First (London) Limited is authorised and regulated in the UK by the Financial Conduct Authority (“FCA”). In the UK, this Document is only being distributed and made available to persons of the kind described in Article 19(5) (investment professionals) and Article 49(2) (high net worth companies, unincorporated associations etc.) of Part IV of the Financial Services and Markets Act 2000 (Financial Promotion) Order 2005 (‘’FPO’’) and any investment activity to which this presentation relates is only available to, and will only be engaged in with, such persons. Persons who do not have professional experience in matters relating to investment or who are not persons to whom Article 49 of the FPO applies should not rely on this document. This Document is only prepared for and available to persons who qualify as Professional Investors under the Markets in Financial Instruments Directive.