How equity-backed loans can meet the liquidity ambitions of Asia’s borrowers

Equity-backed lending is emerging as a compelling funding mechanism in the current environment, and it is worth examining its merits versus other liquidity options - particularly given the rapid growth in the number of potential borrowers in Asia this kind of lending could benefit.

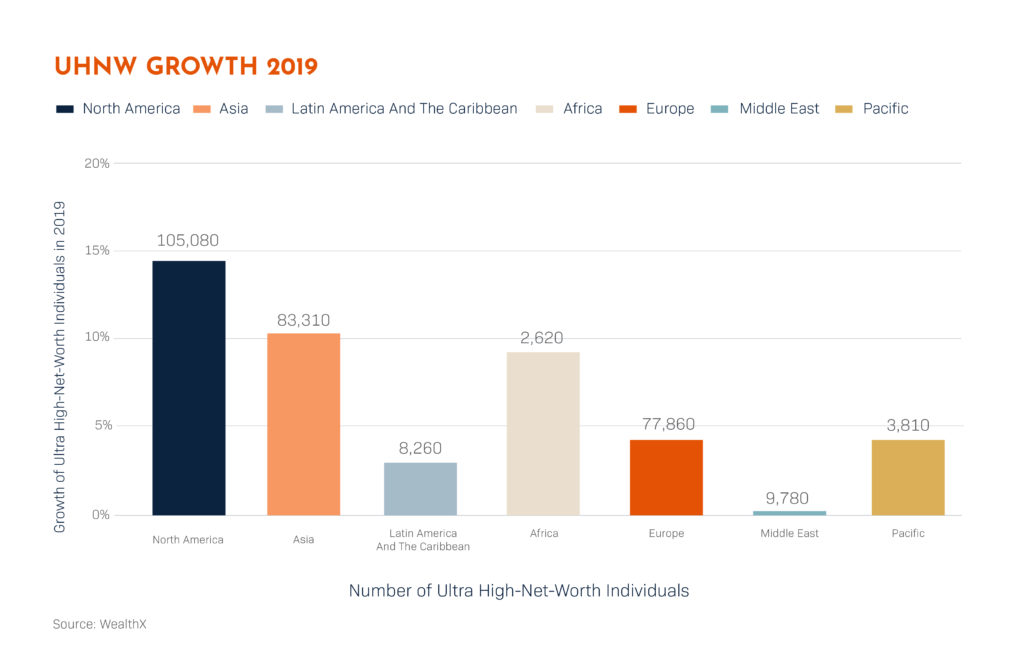

Asia’s ultra-high-net worth (UHNW) population – the second largest behind North America – grew 10.2% to 83,310 individuals in 2019.[1] As economic conditions, and consequent risks and opportunities, shift rapidly, many of these individuals will be looking for new ways to put their assets to work.

Asia 10.2% (83,310) North America 14.5% (105,080)

The premise is relatively simple: equity-backed loans allow investors, typically with concentrated holdings, to use their shares as collateral to unlock liquidity for other needs while still maintaining upside participation in the stock. At times their ambitions are business-oriented. The funds could be used to start a new venture, diversify investment or exercise options due to expire. Other projects are more personal – for example to address tax liabilities or to purchase “crown jewel” assets.

Through our two decades as a specialist in equities-backed lending, we have developed a unique approach that maximizes the potential of this model along two key dimensions - flexibility and efficiency.

Lending with agility

On a global basis, most of our loans average in the US$4 million range. Yet we can vary loan amounts considerably depending on borrower needs and market conditions. In markets such as Hong Kong with high liquidity and concentrations of wealth, the average loan size is many multiples larger. In Australia, the average loan size is just US$1 million, but transaction volume is high. In Europe, average deal sizes fall somewhere in the middle.

We are also able to structure liquidity solutions to the specific needs of each borrower by, for example, increasing or decreasing the tranche size, or adjusting the loan to value (LTV) ratio depending on their requirements.

Several borrowers have worked with us on repeat occasions due to this flexibility. For example, we have provided some borrowers a total of US$30 million in liquidity, but across six separate US$5 million tranches. Not surprisingly, we estimate up to 70% of our transactions are with repeat borrowers. Over the past five years, EquitiesFirst’s Asia offices have closed over $1 billion USD in loan transactions for UHNW individuals.

Value, delivered efficiently

The distinctive aspects of our business model also allow us to offer a quick and seamless experience to our borrowers. While we make sure that we conduct all necessary due diligence, we do not require extensive credit checks. The quality and value of the underlying asset – i.e. the equity the borrower supplies as collateral – mitigates the risk on our side of the transaction.

Interests are aligned during the term of the loan as the borrower’s equity is transferred to become a part of the EquitiesFirst portfolio and we become an investor in the stock alongside the owner. From then on, the borrower is simply required to pay a fixed interest rate - typically significantly lower than standard lending rates - on a quarterly basis; and at the end of the term, repay the loan. Once the principal is repaid, EquitiesFirst returns the same number of shares we received at initiation. This means the borrower retains all economic beneficial ownership, including value appreciation and dividend payments.

This level of efficiency is something that other capital providers, typically banks and other large financial institutions, are simply not in a position to offer. As equity-backed lending is typically a niche component of a large bank’s business at best, internal restrictions and a lack of focus limit their ability to act.

By contrast, as a dedicated equity-backed lender, we have worked for years to streamline and enhance our processes in a way that benefits the parties on both sides of each transaction. With a growing presence in Asia, we stand ready to bring these skills to bear as the region’s rising ranks of affluence seek new means to access the liquidity needed to achieve their goals.

Past performance does not guarantee future returns, and individual returns are not guaranteed or warranted.

This Document is intended solely for accredited investors, sophisticated investors, professional investors, or otherwise qualified investors, as may be required by law or otherwise, and it is not intended for, and should not be used by, persons who do not meet the relevant requirements. The content provided herein is for informational purposes only and is general in nature and not targeted to any specific objective or financial need. The views and opinions expressed in this Document have been prepared by third parties and do not necessarily reflect the views and opinions of EquitiesFirst. EquitiesFirst has not independently examined or verified the information provided herein, and no representation is made that it is accurate or complete. Opinions and information herein are subject to change without notice. The content provided does not constitute an offer to sell (or solicitation of an offer to purchase) any securities, investments, or any financial products (“Offer”). Any such Offer shall only be made through a relevant offering or other documentation which sets forth its material terms and conditions. Nothing contained in this Document shall constitute a recommendation, solicitation, invitation, inducement, promotion, or offer for the purchase or sale of any investment product by Equities First Holdings, LLC or its subsidiaries (collectively, “EquitiesFirst”), nor shall this Document be construed in any way as investment, legal, or tax advice, or as a recommendation, reference, or endorsement by EquitiesFirst. You should seek independent financial advice prior to making an investment decision about a financial product.

This Document contains the intellectual property of EquitiesFirst in the United States and other countries, including, without limitation, their respective logos and other registered and unregistered trademarks and service marks. EquitiesFirst reserves all rights in and to their intellectual property contained in this Document. The Document should not be distributed, published, reproduced or otherwise made available in whole or in part by recipients to any other person and, in particular, should not be distributed to persons in any country where such distribution may lead to a breach of any legal or regulatory requirement.

EquitiesFirst make no representation or warranty with respect to this Document and expressly disclaim any implied warranty under law. You acknowledge that EquitiesFirst is not liable under any circumstances for any direct, indirect, special, consequential, incidental, or punitive damages whatsoever, including, without limitation, any lost profits or lost opportunity, even if EquitiesFirst has been advised of the possibility of such damages.

EquitiesFirst makes the following further statements that may be applicable in the stated jurisdiction:

Australia: Equities First Holdings (Australia) Pty Ltd (ACN: 142 644 399) holds an Australian Financial Services Licence (AFSL Number: 387079). All rights reserved.

The information contained on this Document is intended for persons located in Australia only and classified as a Wholesale Client only as defined in Section 761G of the Corporations Act 2001. The distribution of information to persons outside this criteria may be restricted by law and persons who come into possession of it should seek advice and observe any such restriction.

The material contained in this Document is for information purposes only and should not be construed as an offer or solicitation or recommendation to buy or sell financial products.

The information contained in this Document is intended to be general in nature and is not personal financial product advice. Any advice contained in the Document is general advice only and has been prepared without considering your objectives, financial situation or needs. Before acting on any information, you should consider the appropriateness of the information provided and the nature of the relevant financial product having regard to your objectives, financial situation and needs. You should seek independent financial advice and read the relevant disclosure statements or other offer documents prior to making an investment decision about a financial product.

Forecasts are not guaranteed, and undue reliance should not be placed on them. This information is based on views held by Equities First Holdings (Australia) Pty Ltd as at the publishing date of this material.

Dubai: Equities First Holdings Hong Kong Ltd (DIFC Representative Office) at Gate Precinct Building 4, 6th Floor, Office 7, Dubai International Financial Centre (commercial license number CL7354) is regulated by the Dubai Financial Services Authority (“DFSA”) as a Representative Office (DFSA Firm Reference No.: F008752). All rights reserved.

The material contained in this document is for information purposes only and should not be construed as financial advice, including an offer or solicitation or recommendation to buy or sell financial products. The information contained in this document is intended to be general in nature and any advice contained in this document is general advice only and has been prepared without considering your objectives, financial situation, suitability of the financial products or your needs. Before acting on any information, you should consider the appropriateness of the information provided and the nature of the relevant financial product having regard to your objectives, financial situation and needs. If you do not understand the contents of this document, you should consult an authorised financial adviser.

This document relates to a financial product which is not subject to any form of regulation or approval by the DFSA. The DFSA has no responsibility for reviewing or verifying any documents in connection with this financial product. Accordingly, the DFSA has not approved this document or any other associated documents nor taken any steps to verify the information set out in this document, and has no responsibility for it.

Hong Kong: Equities First Holdings Hong Kong Limited is licensed under the Money Lenders Ordinance (Money Lender’s Licence No. 1493/2025) and to carry on the business of dealing in securities (Type 1 licence) under the Securities and Futures Ordinance (“SFO”) (CE No. BFJ407). This Document has not been reviewed by the Hong Kong Securities and Futures Commission. It is not intended as an offer to sell securities or a solicitation to buy any product managed or provided by Equities First Holdings Hong Kong Limited and is only intended for persons who qualify as Professional Investors under the SFO. This document is not directed to individuals or organizations for whom such offers or invitations would be unlawful or prohibited.

Korea: The foregoing is intended solely for sophisticated investors, professional investors or otherwise qualified investors who have sufficient knowledge and experience in entering into securities financing transactions. It is not intended for, and should not be used by, persons who do not meet those criteria.

United Kingdom: Equities First (London) Limited is authorised and regulated in the UK by the Financial Conduct Authority (“FCA”). In the UK, this Document is only being distributed and made available to persons of the kind described in Article 19(5) (investment professionals) and Article 49(2) (high net worth companies, unincorporated associations etc.) of Part IV of the Financial Services and Markets Act 2000 (Financial Promotion) Order 2005 (‘’FPO’’) and any investment activity to which this presentation relates is only available to, and will only be engaged in with, such persons. Persons who do not have professional experience in matters relating to investment or who are not persons to whom Article 49 of the FPO applies should not rely on this document. This Document is only prepared for and available to persons who qualify as Professional Investors under the Markets in Financial Instruments Directive.