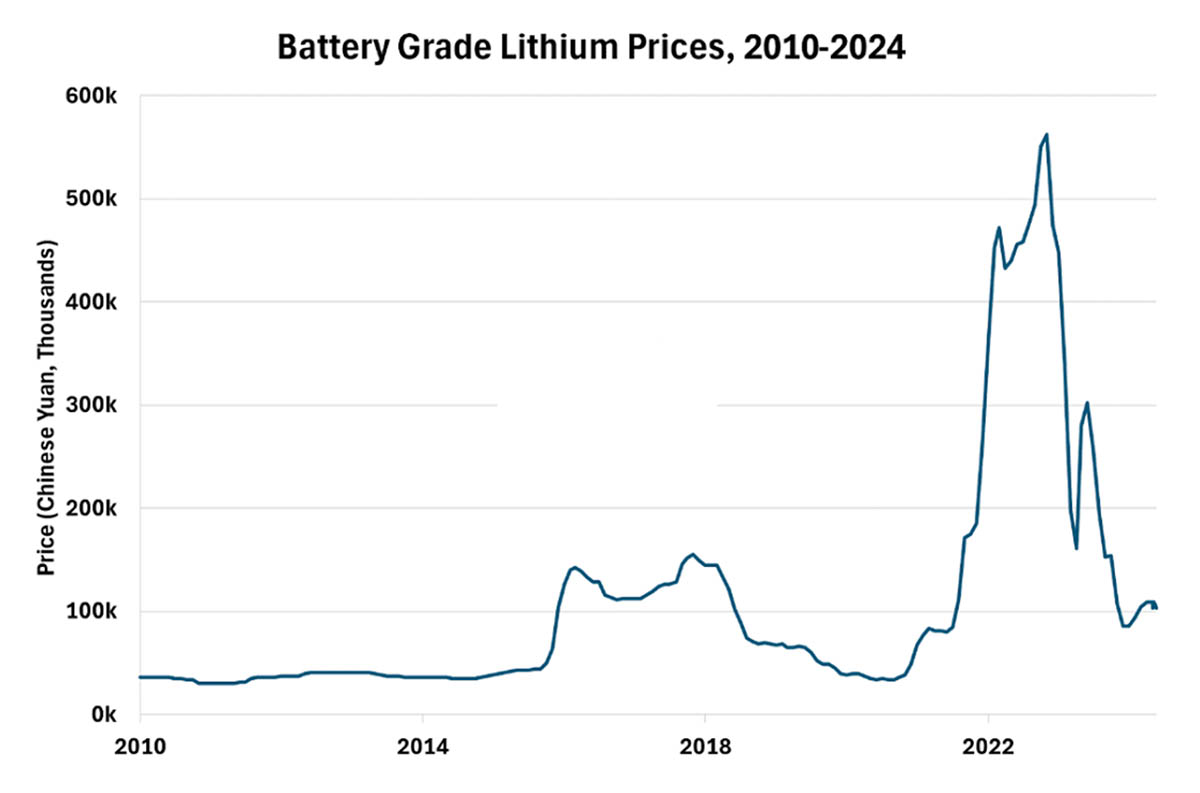

In November 2022, the price of battery-grade lithium carbonate in China — the world’s largest lithium market — briefly touched USD81,000 per tonne before it came crashing back to earth.[1]

Figure 1:

Image source: https://carboncredits.com/understanding-lithium-prices-past-present-and-future/

During those heady days, in 2022, Tesla CEO Elon Musk posted a characteristically feverish tweet: “Price of lithium has gone to insane levels! Tesla might actually have to get into the mining & refining directly at scale, unless costs improve.”[2]

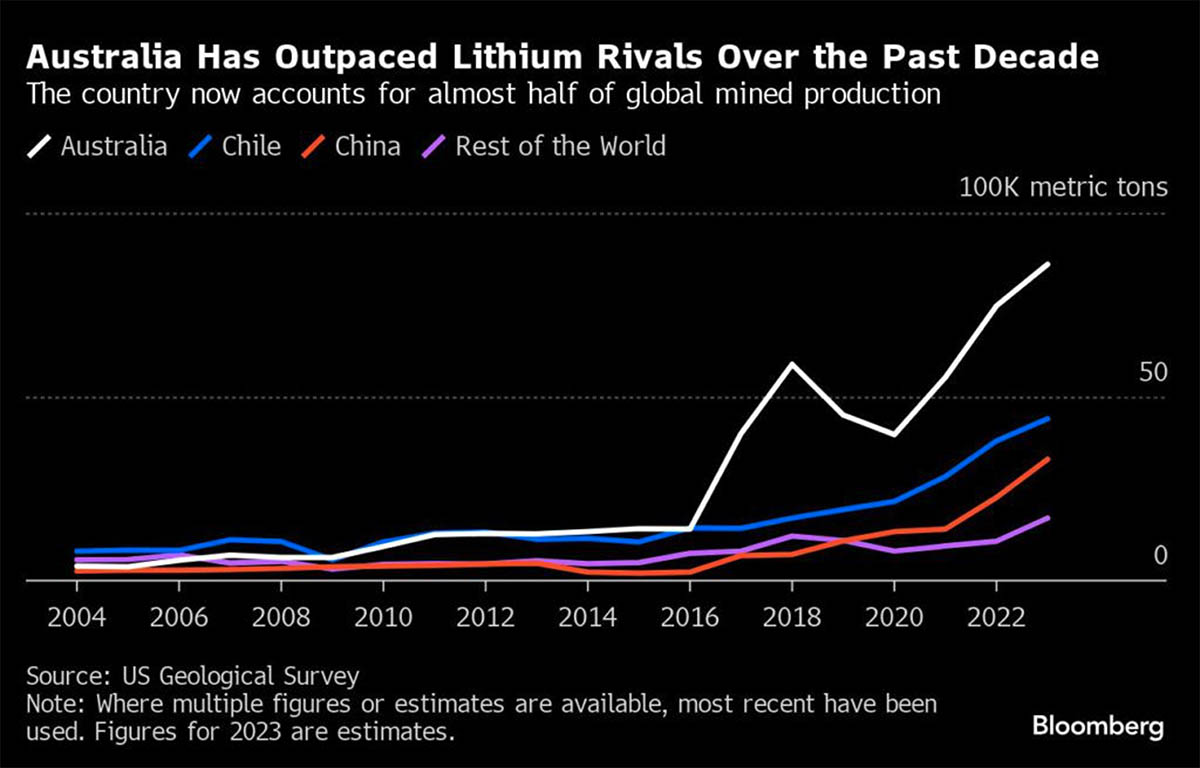

Musk can shelve those diversification plans, with the price back to around USD14,500 per tonne at the end of May 2024.[3] But the repricing has been unwelcome for the resources sector in Australia, the world’s largest producer (see Figure 2) of the metal, which is used in rechargeable batteries for EVs, mobile phones, laptops, digital cameras.

Figure 2:

Taking it in stride

Commodities are known for their wild boom and bust cycles, however, and Australia’s forward-thinking miners remain upbeat about lithium’s prospects given the expected long-term demand for lithium and other critical minerals essential to driving the energy transition.

Pilbara Minerals chief executive Dale Henderson, for example, anticipates a “fairly material” uptick in prices.[4] Heavyweights such as Hancock Prospecting[5] and Mineral Resources[6] have been snapping up lithium assets. And BHP and Rio Tinto have warned that the supply of metals like lithium, nickel, copper, rare earths and aluminum could struggle to keep up with the demands of global decarbonization efforts.[7]

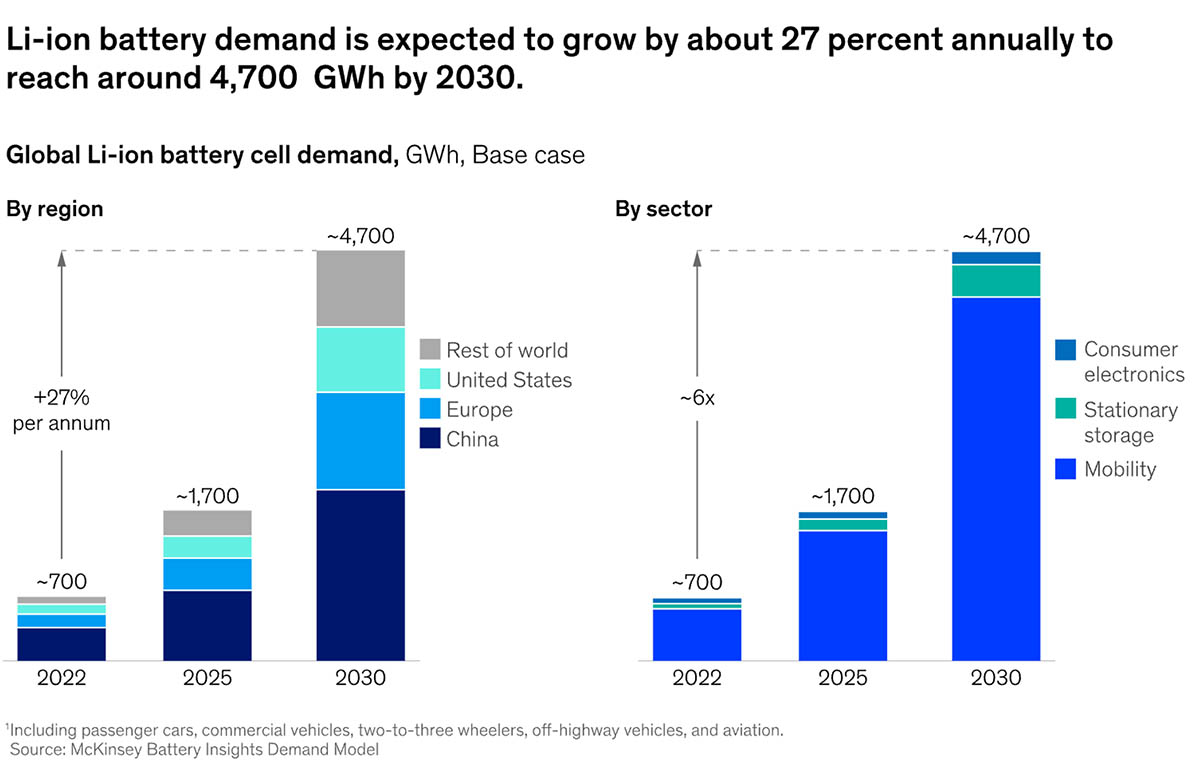

That optimism about lithium, and especially for lithium-ion batteries, goes beyond the mining sector. Consultancy McKinsey foresees a steep and steady increase in demand up to 2030 (see Figure 3).

Figure 3:

Image source: https://www.mckinsey.com/industries/automotive-and-assembly/our-insights/battery-2030-resilient-sustainable-and-circular

In response, Pilbara dug into its cash reserves in Q1 2024 to fund new spending on mine and processing projects in Western Australia.[8] It is also ramping up its processing plant in South Korea. Such investments will be key to countering China's near-monopoly in processing lithium-rich spodumene into the refined materials needed to meet growing demand for batteries.[9]

Meanwhile, though Bank of America’s Head of Metals Research, Michael Widmer, issued a bearish forecast for lithium prices, he revealed in a recent note to clients that “Western producers keep pushing ahead on expectations that lithium demand will expand thanks to policies.”[10]

The Australian Government’s recently introduced Critical Minerals Production Tax Incentives commits A$7 billion over the coming decade to bolster the processing of critical minerals.[11] In the US, the Inflation Reduction Act provides sizeable incentives to expand manufacturing of EVs in America.[12] Policies like these could bolster lithium’s outlook over the next few years. There have also been calls for the Australian government to step in and support the lithium sector by establishing a strategic reserve.[13]

Calling the bottom

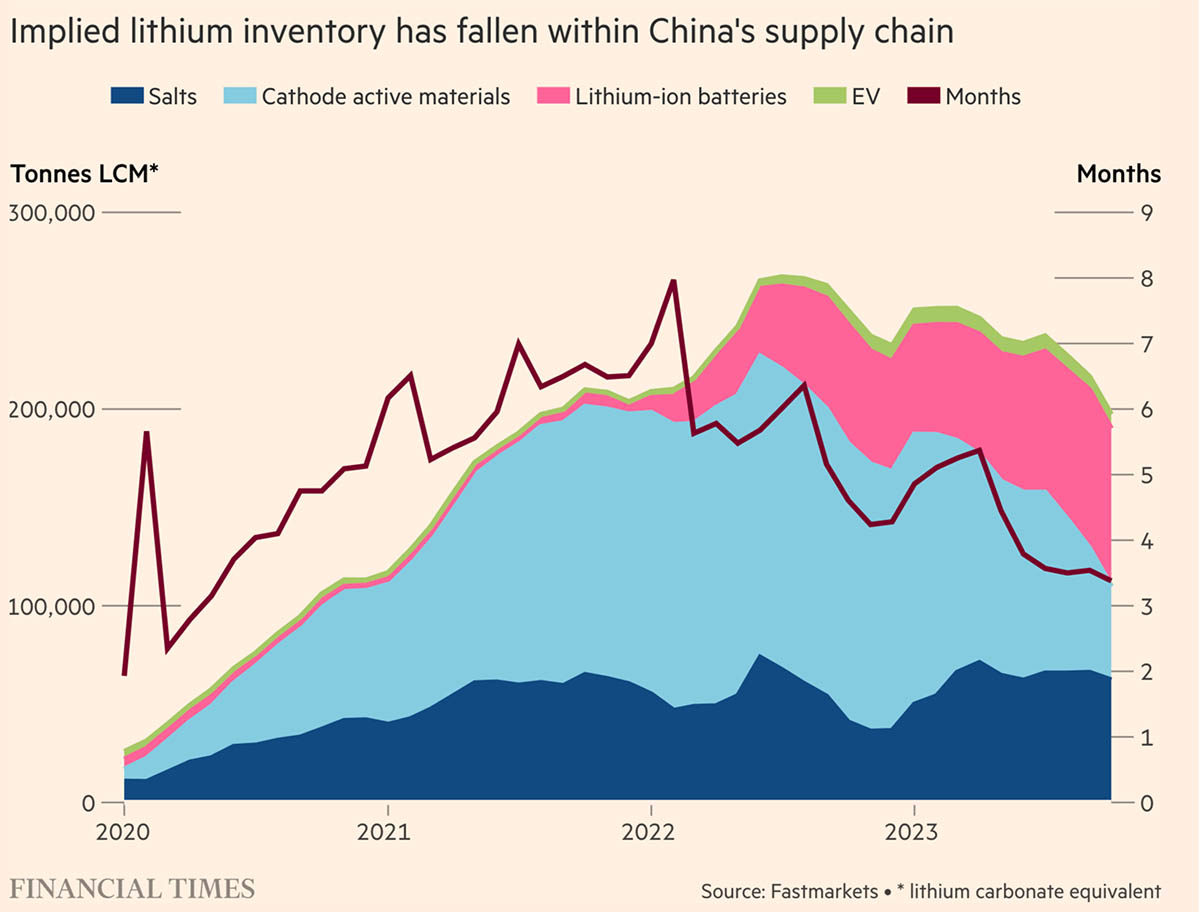

There is a growing sense that financial analysts have got it wrong on lithium, and that rather than facing chronic oversupply, the market could soon even be undersupplied.[14] There are already signs that inventories are thinning (see Figure 4). Moreover, a significant acceleration of investment in green technologies could lead to swift and sustained support for prices.

Figure 4:

Image source: https://www.ft.com/content/0fb27a1a-d149-4d66-87cf-a1e3feecb5e5

For some, the biggest lesson from recent price swings is that the industry needs a more stable supply of lithium to ensure its healthy development.[15] Therefore, while a few miners have sought to cut costs and scale back expansion plans, those who never lost faith in the metal are seeking liquidity to fund continued investment in capacity both upstream and downstream.

Funding those investments, however, has become more difficult.

Australia’s big four banks have slashed their exposure to the domestic resources sector to a decade low because of diminished risk appetite and an erosion of in-house talent equipped to cater to the needs of the mining industry.[16] Take Commonwealth Bank, where total committed exposure to resources has slumped from almost A$17 billion to A$7 billion between 2015 and 2022.[17]

Turning to alternative financing

This has led Australia’s critical minerals producers to turn to alternative sources of financing, including end consumers, shareholder equity, government funding and export credit agencies.[18] At EquitiesFirst, we have also seen strong demand for liquidity from our own Australian clients, including from long-term shareholders in the resources sector.

Australia’s miners are not alone in pursuing additional capacity. China’s top lithium firms, too, are confident about long-term prospects, looking past their near-term profit slump to pursue expansion.[19] Indian companies are in search of lithium investments around the world, including in Australia.[20] And, of course, Chilean lithium giant SQM is undertaking an aggressive expansion in Australia.[21]

At a time when traditional lenders are wary about Australia’s resources sector, entrepreneurs with an eye on the longer game remain confident. Specialty financing, including equities-backed financing, could play a role in supporting the sector’s development and helping to maintain a steady supply of the critical minerals needed to keep the world on track to net zero.

[1] https://carboncredits.com/why-lithium-prices-are-plunging-and-what-to-expect/#:~:text=The%20Steep%20Decline%20in%20Lithium%20Prices&text=Lithium%20carbonate%20prices%20have%20experienced,decrease%20year%2Don%2Dyear.

[2] https://www.bloomberg.com/news/articles/2022-04-08/tesla-may-start-mining-lithium-as-musk-cites-battery-metal-cost

[3] https://www.fastmarkets.com/insights/china-lithium-spot-prices-inch-down/

[4] https://www.afr.com/companies/mining/pilbara-minerals-calls-fairly-material-uptick-in-lithium-prices-20240419-p5fl2f

[5] https://www.australianmining.com.au/will-rinehart-drum-up-another-lithium-frenzy/

[6] https://www.australianmining.com.au/minres-strikes-hot-on-lithium

[7] https://www.afr.com/companies/mining/bank-exposure-to-resources-sector-crashes-to-decade-low-20230316-p5csvi

[8] https://www.afr.com/companies/mining/pilbara-minerals-calls-fairly-material-uptick-in-lithium-prices-20240419-p5fl2f

[9] https://www.bloomberg.com/news/articles/2024-04-25/ev-batteries-miners-are-betting-lithium-could-be-a-green-lifeline-for-australia

[10] https://www.afr.com/markets/commodities/bank-of-america-slashes-lithium-price-forecasts-for-2024-2025-20240201-p5f1i8

[11] https://www.mining-technology.com/news/australia-tax-critical-minerals/#:~:text=Australia%20commits%20A%247bn%20to%20tax%20incentive%20for%20critical,cobalt%2C%20nickel%20and%20rare%20earths.

[12] https://chicagopolicyreview.org/2023/01/26/the-inflation-reduction-acts-big-bet-on-electric-vehicles/

[13] https://www.afr.com/companies/mining/australia-can-save-the-global-lithium-industry-from-the-chinese-state-20240205-p5f2dc

[14] https://www.afr.com/markets/commodities/this-fund-is-betting-wall-street-banks-have-lithium-slump-call-wrong-20240404-p5fhfz

[15] https://news.bloomberglaw.com/private-equity/the-lithium-world-confronts-hard-truths-after-epic-boom-and-bust

[16] https://www.afr.com/companies/mining/bank-exposure-to-resources-sector-crashes-to-decade-low-20230316-p5csvi#:~:text=The%20big%20four%20banks'%20exposure,in%20%E2%80%9Cfuture%20facing%E2%80%9D%20commodities.

[17] https://www.afr.com/companies/mining/bank-exposure-to-resources-sector-crashes-to-decade-low-20230316-p5csvi#:~:text=The%20big%20four%20banks'%20exposure,in%20%E2%80%9Cfuture%20facing%E2%80%9D%20commodities.

[18] https://www.afr.com/companies/mining/bank-exposure-to-resources-sector-crashes-to-decade-low-20230316-p5csvi#:~:text=The%20big%20four%20banks'%20exposure,in%20%E2%80%9Cfuture%20facing%E2%80%9D%20commodities.

[19] https://www.bloomberg.com/news/articles/2024-04-01/top-china-lithium-firms-look-past-profit-slump-and-vow-expansion

[20] https://www.business-standard.com/companies/news/khanij-bidesh-india-likely-to-acquire-lithium-asset-in-australia-in-fy25-124051100323_1.html

[21] https://www.afr.com/companies/mining/chilean-lithium-giant-flags-aggressive-australian-expansion-20240307-p5fajw