Climate innovation needs more than bank and venture funding

By 2025, the world is set to generate more electricity from renewable energy than from coal – a major step on the road to a low-carbon future.[1]

Still, several other pieces need to fall into place to solve the decarbonization puzzle. The International Energy Agency (IEA) estimates that around 35% of emissions reductions needed to reach net zero by 2050 will need to come from technologies that have yet to be commercially deployed.[2]

Scaling up climate tech, therefore, is a historic investment opportunity. Yet accessing capital for these emerging business models remains a challenge because they are not yet cost-competitive. Take sustainable aviation fuel, which is about 2.5X more expensive than regular jet fuel.[3] Or green hydrogen, produced from electrolysis of water using renewable energy, which currently costs up to 12X as much as widely used gray hydrogen, produced using natural gas in a process that gives off carbon dioxide.[4]

Over time, costs are expected to decline rapidly as technologies scale. BloombergNEF forecasts green hydrogen will undercut gray in most of the world by 2035, for example.[5]

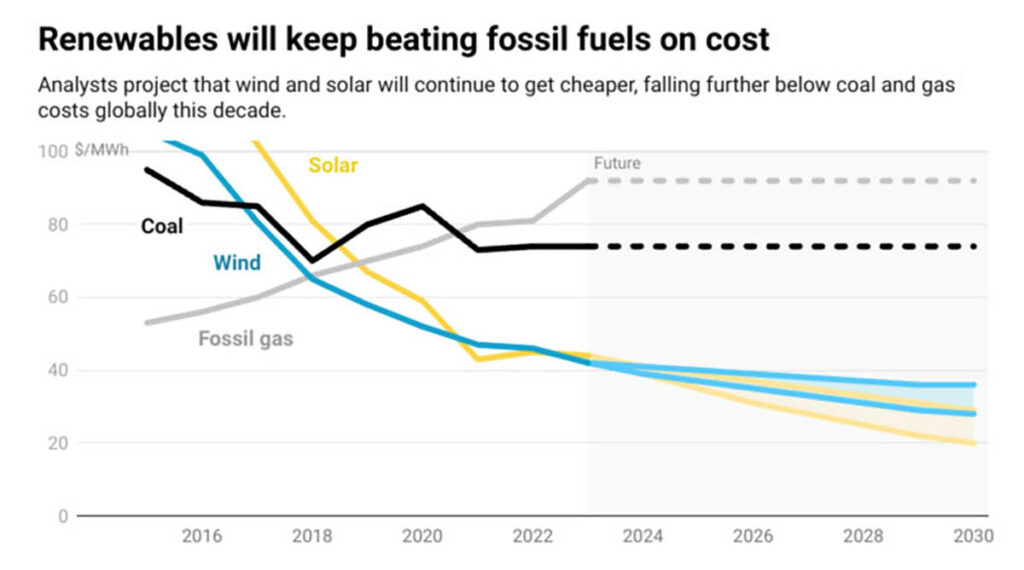

This mirrors the trajectory of renewable power. The global weighted average cost of solar and onshore wind energy plunged 89% and 69%, respectively, between 2010 and 2022.[6] That followed on from decades of steep cost reductions, which have made solar and wind cost-competitive with fossil fuels.

Figure 1: Costs of solar, wind, coal and fossil gas

Reaching those economies of scale, however, is only possible if more investment flows into the sector. That will require easier access to funding.

Funding climate tech

While early-stage investments may have been relatively easy to come by when interest rates were low, the change in the rate environment since 2022 has led to tighter liquidity conditions and an overall decline in startup valuations.

Across more than a thousand deals tracked by BloombergNEF in 2023, climate tech companies raised US$51 billion in venture capital and private equity funding, 12% lower than the previous year.[7] Many climate tech projects have reportedly been forced to shut down because of the harsher funding environment.[8]

Moreover, while venture funding is well suited for seeing startups through the initial – riskier – tech iteration phase of their journeys, when it comes time to deploy proven assets at scale, other types of funding are often needed.[9] These, too, have become harder to access following the adoption of tighter lending standards by traditional lenders. Even if banks are willing to lend, they typically impose onerous restrictions on how those funds can be used.

Compared to startups developing software, climate tech firms usually require significantly higher capital at early stages and often take longer to break even.

The ongoing difficulty in accessing funding could lead to several startups with viable technologies being unable to see them through to commercialization. In addition to potentially setting back the world’s climate objectives, this could lead to considerable foregone commercial opportunities.

All this points to a growing role for alternative capital, including private credit and specialty finance, in providing the flexible funding needed for business owners to accelerate their deployment of low-carbon technologies.

Emerging opportunities

Within the climate tech category, there are several opportunities worth highlighting for early-stage investors, according to PitchBook research. The main one is the carbon-tech segment, including carbon-capture startups and firms developing software for emissions measurement and accounting.[10] The next three most attractive segments are: electric vehicles, technologies to reduce emissions in the manufacturing process, and land use solutions to tackle sustainability in agriculture and forestry.

BloombergNEF, meanwhile, identified startups in three main categories in its latest Pioneers competition, with results announced in April 2024:[11]

Relieving clean-power bottlenecks, primarily using software to identify the best sites for projects, deal with peaks and troughs in renewable generation and manage battery storage.

Decarbonizing buildings with solutions to build or retrofit properties with more energy efficient systems for heating, cooling and lighting. Often, these can make living and working spaces more comfortable, too.

New net-zero fuels, especially focused on aviation, shipping and long-distance trucking, which will be hard to electrify because batteries are not light or powerful enough to meet their needs.

Despite the risks involved in investing in these and other emerging climate tech, there is clearly strong return potential, especially given the likelihood that support for the climate tech sector – from governments[12] and businesses[13] – could ramp up significantly as the need to address climate change becomes more urgent.

In particular, as businesses face higher implicit costs of emitting greenhouse gases by way of carbon taxes – which are expected to surge over the coming years[14] – the value of technologies designed to reduce emissions will rise in tandem.

Ahead of that, however, even proven climate technologies are at risk of falling by the wayside because of the current funding situation. Specialty financing could help bridge the gap. Monetizing long-term shareholdings, for example, can give qualified investors an alternative source of funding for climate tech initiatives.

Given the scale of the global energy transition, it’s clear that every form of capital will have a part to play.

Past performance does not guarantee future returns, and individual returns are not guaranteed or warranted.

This Document is intended solely for accredited investors, sophisticated investors, professional investors, or otherwise qualified investors, as may be required by law or otherwise, and it is not intended for, and should not be used by, persons who do not meet the relevant requirements. The content provided herein is for informational purposes only and is general in nature and not targeted to any specific objective or financial need. The views and opinions expressed in this Document have been prepared by third parties and do not necessarily reflect the views and opinions of EquitiesFirst. EquitiesFirst has not independently examined or verified the information provided herein, and no representation is made that it is accurate or complete. Opinions and information herein are subject to change without notice. The content provided does not constitute an offer to sell (or solicitation of an offer to purchase) any securities, investments, or any financial products (“Offer”). Any such Offer shall only be made through a relevant offering or other documentation which sets forth its material terms and conditions. Nothing contained in this Document shall constitute a recommendation, solicitation, invitation, inducement, promotion, or offer for the purchase or sale of any investment product by Equities First Holdings, LLC or its subsidiaries (collectively, “EquitiesFirst”), nor shall this Document be construed in any way as investment, legal, or tax advice, or as a recommendation, reference, or endorsement by EquitiesFirst. You should seek independent financial advice prior to making an investment decision about a financial product.

This Document contains the intellectual property of EquitiesFirst in the United States and other countries, including, without limitation, their respective logos and other registered and unregistered trademarks and service marks. EquitiesFirst reserves all rights in and to their intellectual property contained in this Document. The Document should not be distributed, published, reproduced or otherwise made available in whole or in part by recipients to any other person and, in particular, should not be distributed to persons in any country where such distribution may lead to a breach of any legal or regulatory requirement.

EquitiesFirst make no representation or warranty with respect to this Document and expressly disclaim any implied warranty under law. You acknowledge that EquitiesFirst is not liable under any circumstances for any direct, indirect, special, consequential, incidental, or punitive damages whatsoever, including, without limitation, any lost profits or lost opportunity, even if EquitiesFirst has been advised of the possibility of such damages.

EquitiesFirst makes the following further statements that may be applicable in the stated jurisdiction:

Australia: Equities First Holdings (Australia) Pty Ltd (ACN: 142 644 399) holds an Australian Financial Services Licence (AFSL Number: 387079). All rights reserved.

The information contained on this Document is intended for persons located in Australia only and classified as a Wholesale Client only as defined in Section 761G of the Corporations Act 2001. The distribution of information to persons outside this criteria may be restricted by law and persons who come into possession of it should seek advice and observe any such restriction.

The material contained in this Document is for information purposes only and should not be construed as an offer or solicitation or recommendation to buy or sell financial products.

The information contained in this Document is intended to be general in nature and is not personal financial product advice. Any advice contained in the Document is general advice only and has been prepared without considering your objectives, financial situation or needs. Before acting on any information, you should consider the appropriateness of the information provided and the nature of the relevant financial product having regard to your objectives, financial situation and needs. You should seek independent financial advice and read the relevant disclosure statements or other offer documents prior to making an investment decision about a financial product.

Forecasts are not guaranteed, and undue reliance should not be placed on them. This information is based on views held by Equities First Holdings (Australia) Pty Ltd as at the publishing date of this material.

Dubai: Equities First Holdings Hong Kong Ltd (DIFC Representative Office) at Gate Precinct Building 4, 6th Floor, Office 7, Dubai International Financial Centre (commercial license number CL7354) is regulated by the Dubai Financial Services Authority (“DFSA”) as a Representative Office (DFSA Firm Reference No.: F008752). All rights reserved.

The material contained in this document is for information purposes only and should not be construed as financial advice, including an offer or solicitation or recommendation to buy or sell financial products. The information contained in this document is intended to be general in nature and any advice contained in this document is general advice only and has been prepared without considering your objectives, financial situation, suitability of the financial products or your needs. Before acting on any information, you should consider the appropriateness of the information provided and the nature of the relevant financial product having regard to your objectives, financial situation and needs. If you do not understand the contents of this document, you should consult an authorised financial adviser.

This document relates to a financial product which is not subject to any form of regulation or approval by the DFSA. The DFSA has no responsibility for reviewing or verifying any documents in connection with this financial product. Accordingly, the DFSA has not approved this document or any other associated documents nor taken any steps to verify the information set out in this document, and has no responsibility for it.

Hong Kong: Equities First Holdings Hong Kong Limited is licensed under the Money Lenders Ordinance (Money Lender’s Licence No. 1493/2025) and to carry on the business of dealing in securities (Type 1 licence) under the Securities and Futures Ordinance (“SFO”) (CE No. BFJ407). This Document has not been reviewed by the Hong Kong Securities and Futures Commission. It is not intended as an offer to sell securities or a solicitation to buy any product managed or provided by Equities First Holdings Hong Kong Limited and is only intended for persons who qualify as Professional Investors under the SFO. This document is not directed to individuals or organizations for whom such offers or invitations would be unlawful or prohibited.

Korea: The foregoing is intended solely for sophisticated investors, professional investors or otherwise qualified investors who have sufficient knowledge and experience in entering into securities financing transactions. It is not intended for, and should not be used by, persons who do not meet those criteria.

United Kingdom: Equities First (London) Limited is authorised and regulated in the UK by the Financial Conduct Authority (“FCA”). In the UK, this Document is only being distributed and made available to persons of the kind described in Article 19(5) (investment professionals) and Article 49(2) (high net worth companies, unincorporated associations etc.) of Part IV of the Financial Services and Markets Act 2000 (Financial Promotion) Order 2005 (‘’FPO’’) and any investment activity to which this presentation relates is only available to, and will only be engaged in with, such persons. Persons who do not have professional experience in matters relating to investment or who are not persons to whom Article 49 of the FPO applies should not rely on this document. This Document is only prepared for and available to persons who qualify as Professional Investors under the Markets in Financial Instruments Directive.