How demand from China is underpinning gold’s continued ascent

14 November 2024

For months, analysts have been speculating whether the price of gold can keep rising. So far, the answer has been ‘yes’.

But what are the forces underpinning this steady rise – and will they continue? From the start of 2024 until November, gold was up 34%, to about USD2,700 per troy ounce. And according to Goldman Sachs Commodities Strategist Lina Thomas, it will reach USD3,000 by the end of 2025.[1]

Expectations of continued interest rate cuts will doubtless play an important part in this dynamic. Traditionally, lower rates have boded well for gold. Because the precious metal does not offer a yield, it can become less attractive when interest rates are higher, sending investors to interest-bearing assets like bonds.

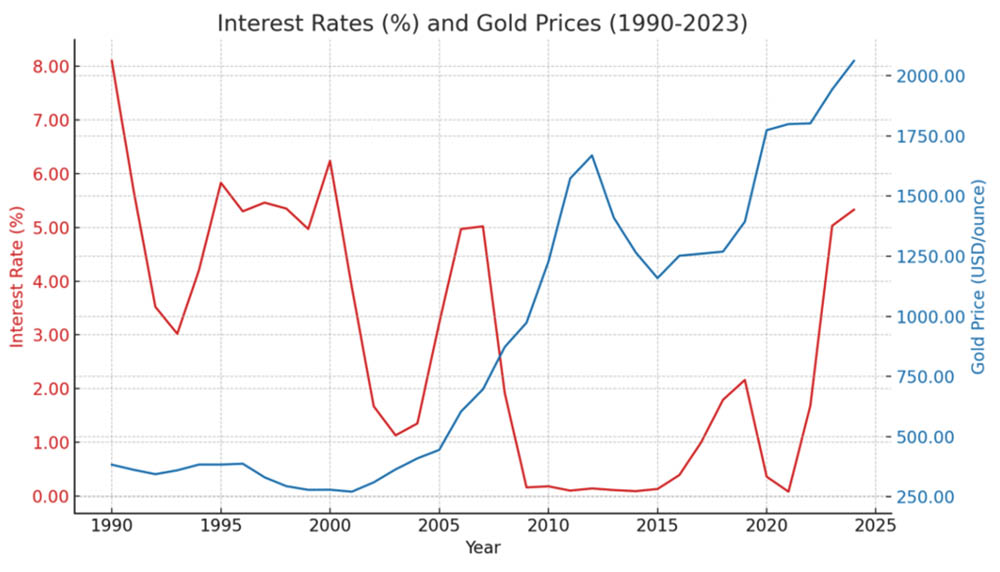

But interest rates are just one of the many determinants of the price of gold. After all, although the inverse relationship between gold prices and interest rates seemed to hold from 1990 to 2016 (see Figure 1), between 2016 and 2019 gold prices kept rising even though interest rates also climbed consistently.[2] Since then, gold has continued to appreciate even as central banks slashed interest rates during the Covid-19 era and then embarked on a tightening cycle to rein in inflation.[3]

Figure 1: Interest rates and gold prices, 1990-2023[4]

So, while gold price movements cannot be explained by interest rates movements alone, the start of an easing cycle is clearly a tailwind.

Then there is the current environment of heightened geopolitical tensions and global macroeconomic uncertainty, a combination that tends to stoke demand for haven assets like gold. The long wait for the US presidential election is now over, but ongoing hot wars in Europe and the Middle East, along with the threat of intensifying trade wars pitting China against the US and the European Union, will keep investors on edge for the foreseeable future.

Central banks underpin demand

However, there is another major long-term driver of demand for gold that could potentially play an even bigger role in sustaining its upward trajectory: purchases by the People’s Bank of China (PBoC) to replace the US Treasuries that currently make up about a third of its reserves,[5] against a backdrop of escalating trade tensions between the two nations.

Policymakers may also increasingly want to lessen their exposure to fiscal risks in the US, where borrowing stands at about USD35 trillion, equivalent to about 124% of GDP.[6]

Central banks and sovereign wealth funds in Russia and the Middle East are also following this trend. Aware of these dynamics, US funds, family offices and asset managers have also reportedly increased gold’s allocation within their portfolios to 10-15% from 5-7%.[7]

China has been the primary driver of the price of gold in the last two years, according to Bloomberg, having purchased more than 2,800 tons from abroad during the period, more than the amount underpinning exchange-traded funds (ETFs).[8]

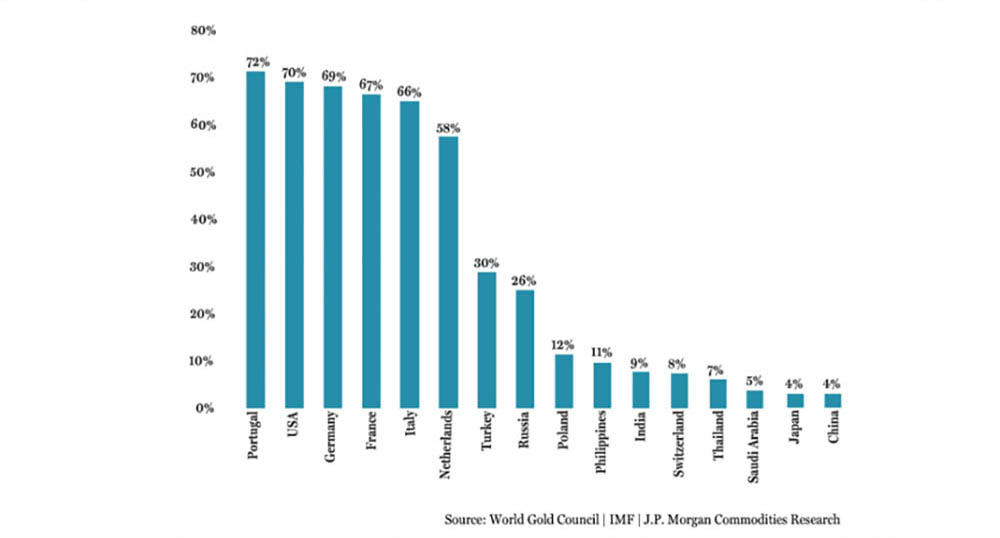

Gold now accounts for nearly 5% of China’s total reserves, but that still pales in comparison to the near 70% share held by the US Federal Reserve (see Figure 2) and other Western countries, suggesting much further room for the PBoC’s gold purchases to run.[9]

Figure 2: Gold as a percentage of central bank reserves

Chinese retail investors have also amassed gold over the past two years to counter headwinds in other assets, such as property and equities.[10] Although the high price is putting a short-term crimp on demand from Chinese retail investors and jewelry buyers,[11] that could prove transitory if prices look set to stay high.

There are good reasons still to be wary: gold’s sharp rise could mean that it is poised for a sharp correction. But analysts point out that there are plenty of buyers waiting in the wings to buy dips and sustain the upward trajectory.[12]

Even though the pace of central bank gold purchases has moderated recently, that slowdown could prove temporary. In any case, it is likely to be offset by gold holdings in Western exchange-traded funds gradually increasing as interest rates fall, according to Goldman Sachs Research.[13] For this reason, most other major brokerages predict gold’s record-breaking price rally will extend into 2025.[14]

Longer term, gold’s fortunes will depend on how quickly countries will choose to replace US Treasuries in their reserves, which, in turn, will depend heavily on the evolving geopolitical landscape and how much further the US economy slows.[15]

The US dollar’s share of global foreign exchange reserves has dropped by about 10 percentage points since the turn of the century.[16] That process could accelerate as viable alternatives emerge. Central banks have been replacing dollars with not only currencies of very large economies such as China and the European Union, but, increasingly, also currencies from smaller economies with strong credit ratings, like Australia, Canada and South Korea.[17]

Shelter in the storm

Throughout history, people have sought out gold as a way to preserve wealth in times of upheaval and strife. That function could well see it continue to test new highs as the world continues to grapple with geopolitical and macroeconomic uncertainty.

In such an environment, securities-backed financing from EquitiesFirst shows its worth, allowing investors to generate stable capital without having to sacrifice the upside potential of their underlying holdings. They can thereby follow their convictions in managing volatility while seeking to preserve and grow their wealth.

Past performance does not guarantee future returns, and individual returns are not guaranteed or warranted.

This Document is intended solely for accredited investors, sophisticated investors, professional investors, or otherwise qualified investors, as may be required by law or otherwise, and it is not intended for, and should not be used by, persons who do not meet the relevant requirements. The content provided herein is for informational purposes only and is general in nature and not targeted to any specific objective or financial need. The views and opinions expressed in this Document have been prepared by third parties and do not necessarily reflect the views and opinions of EquitiesFirst. EquitiesFirst has not independently examined or verified the information provided herein, and no representation is made that it is accurate or complete. Opinions and information herein are subject to change without notice. The content provided does not constitute an offer to sell (or solicitation of an offer to purchase) any securities, investments, or any financial products (“Offer”). Any such Offer shall only be made through a relevant offering or other documentation which sets forth its material terms and conditions. Nothing contained in this Document shall constitute a recommendation, solicitation, invitation, inducement, promotion, or offer for the purchase or sale of any investment product by Equities First Holdings, LLC or its subsidiaries (collectively, “EquitiesFirst”), nor shall this Document be construed in any way as investment, legal, or tax advice, or as a recommendation, reference, or endorsement by EquitiesFirst. You should seek independent financial advice prior to making an investment decision about a financial product.

This Document contains the intellectual property of EquitiesFirst in the United States and other countries, including, without limitation, their respective logos and other registered and unregistered trademarks and service marks. EquitiesFirst reserves all rights in and to their intellectual property contained in this Document. The Document should not be distributed, published, reproduced or otherwise made available in whole or in part by recipients to any other person and, in particular, should not be distributed to persons in any country where such distribution may lead to a breach of any legal or regulatory requirement.

EquitiesFirst make no representation or warranty with respect to this Document and expressly disclaim any implied warranty under law. You acknowledge that EquitiesFirst is not liable under any circumstances for any direct, indirect, special, consequential, incidental, or punitive damages whatsoever, including, without limitation, any lost profits or lost opportunity, even if EquitiesFirst has been advised of the possibility of such damages.

EquitiesFirst makes the following further statements that may be applicable in the stated jurisdiction:

Australia: Equities First Holdings (Australia) Pty Ltd (ACN: 142 644 399) holds an Australian Financial Services Licence (AFSL Number: 387079). All rights reserved.

The information contained on this Document is intended for persons located in Australia only and classified as a Wholesale Client only as defined in Section 761G of the Corporations Act 2001. The distribution of information to persons outside this criteria may be restricted by law and persons who come into possession of it should seek advice and observe any such restriction.

The material contained in this Document is for information purposes only and should not be construed as an offer or solicitation or recommendation to buy or sell financial products.

The information contained in this Document is intended to be general in nature and is not personal financial product advice. Any advice contained in the Document is general advice only and has been prepared without considering your objectives, financial situation or needs. Before acting on any information, you should consider the appropriateness of the information provided and the nature of the relevant financial product having regard to your objectives, financial situation and needs. You should seek independent financial advice and read the relevant disclosure statements or other offer documents prior to making an investment decision about a financial product.

Forecasts are not guaranteed, and undue reliance should not be placed on them. This information is based on views held by Equities First Holdings (Australia) Pty Ltd as at the publishing date of this material.

Dubai: Equities First Holdings Hong Kong Ltd (DIFC Representative Office) at Gate Precinct Building 4, 6th Floor, Office 7, Dubai International Financial Centre (commercial license number CL7354) is regulated by the Dubai Financial Services Authority (“DFSA”) as a Representative Office (DFSA Firm Reference No.: F008752). All rights reserved.

The information contained in this document is intended to be general in nature, and, to the extent that it is perceived as advice, any advice contained in this document is general advice only and has been prepared without considering your objectives, financial situation, suitability of the financial products or your needs.

The material contained in this document is for information purposes only and should not be construed as financial advice, including an offer or solicitation or recommendation to buy or sell financial products. The information contained in this document is intended to be general in nature and any advice contained in this document is general advice only and has been prepared without considering your objectives, financial situation, suitability of the financial products or your needs. Before acting on any information, you should consider the appropriateness of the information provided and the nature of the relevant financial product having regard to your objectives, financial situation and needs. If you do not understand the contents of this document, you should consult an authorised financial adviser.

This document relates to a financial product which is not subject to any form of regulation or approval by the DFSA. The DFSA has no responsibility for reviewing or verifying any documents in connection with this financial product. Accordingly, the DFSA has not approved this document or any other associated documents nor taken any steps to verify the information set out in this document, and has no responsibility for it.

Hong Kong: Equities First Holdings Hong Kong Limited is licensed under the Money Lenders Ordinance (Money Lender’s Licence No. 1659/2024) and to carry on the business of dealing in securities (Type 1 licence) under the Securities and Futures Ordinance (“SFO”) (CE No. BFJ407). This Document has not been reviewed by the Hong Kong Securities and Futures Commission. It is not intended as an offer to sell securities or a solicitation to buy any product managed or provided by Equities First Holdings Hong Kong Limited and is only intended for persons who qualify as Professional Investors under the SFO. This document is not directed to individuals or organizations for whom such offers or invitations would be unlawful or prohibited.

Korea: The foregoing is intended solely for sophisticated investors, professional investors or otherwise qualified investors who have sufficient knowledge and experience in entering into securities financing transactions. It is not intended for, and should not be used by, persons who do not meet those criteria.

United Kingdom: Equities First (London) Limited is authorised and regulated in the UK by the Financial Conduct Authority (“FCA”). In the UK, this Document is only being distributed and made available to persons of the kind described in Article 19(5) (investment professionals) and Article 49(2) (high net worth companies, unincorporated associations etc.) of Part IV of the Financial Services and Markets Act 2000 (Financial Promotion) Order 2005 (‘’FPO’’) and any investment activity to which this presentation relates is only available to, and will only be engaged in with, such persons. Persons who do not have professional experience in matters relating to investment or who are not persons to whom Article 49 of the FPO applies should not rely on this document. This Document is only prepared for and available to persons who qualify as Professional Investors under the Markets in Financial Instruments Directive.