Australia: navigating post-IPO escrow for key employees

"These are exciting times for investors in Australian Initial Public Offerings (IPO) – especially key employees who hold Founder Shares. These employees often look to sell these shares as soon as the post-IPO escrow period ends. However, there is an alternative that enables them to raise funds while retaining exposure to their vested shares" - says Mitchell Hopwood at EquitiesFirst.

The last 12 months have been very difficult for humanity, but great for markets. After collapsing in the first quarter of 2020, global stocks have come roaring back faster and further than almost anyone expected. In April this year, the Dow Jones Industrial average crossed the 34,000 point mark for the first time.1 Here in Australia, the ASX200 breached 7,000 points for the first time since the pandemic began, coming within range of its all-time high.2

This extraordinary recovery in equities has been fuelled by unprecedented fiscal stimulus and monetary easing intended to cushion the impact of the worst economic crisis since the Second World War. In recent months, demand for stocks has been supercharged by growing optimism that the rollout of vaccines heralds a gradual return to pre-pandemic life around the world.

Bumper Crop of IPOs

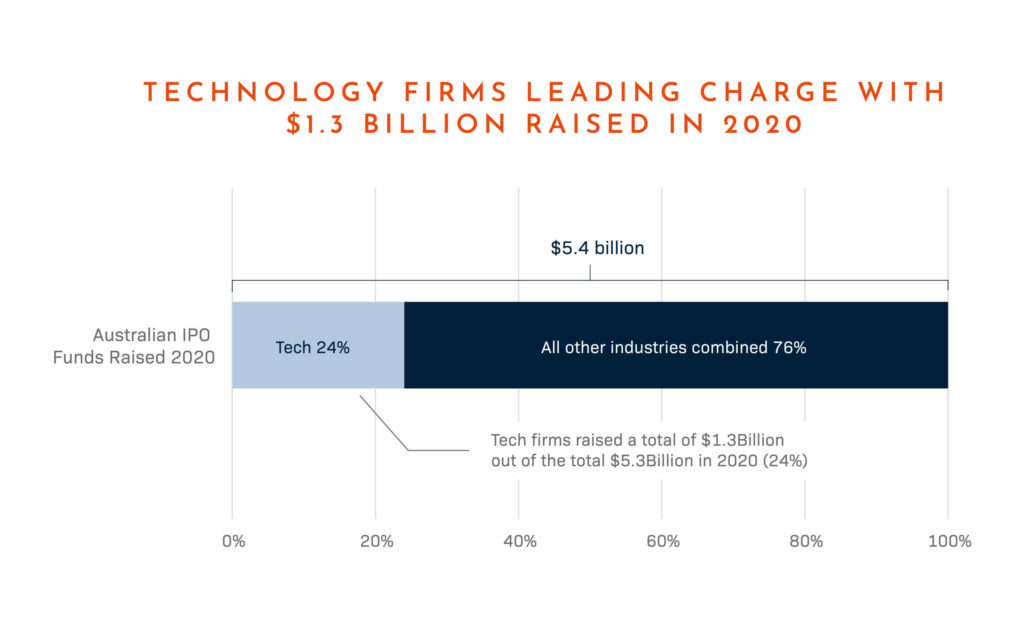

Not surprisingly, companies have been rushing to list in such buoyant markets, with analysts expecting another bumper year for Australia IPOs in 2021. It is also no surprise, given the shifts the pandemic has caused to how we work and live, that technology firms have been leading the charge. According to Bloomberg, they accounted for A$1.3 billion of the total A$5.4 billion raised through floats last year, achieving the sector’s biggest share of IPO volumes in at least 10 years.3

There were 66 IPOs in Australia’s 2020 vintage. Investors in these newly-listed companies have generally done well: they were up an average of 42% at the end of the year and markets have continued to rise since then.4 This performance has helped create wealth for employees who received share options ahead of those companies’ IPOs, among other shareholders. For employee shareholders of information technology stocks, the wealth effect has been even more pronounced: shares in this sector have returned more than 86% in the last 12 months.5

Tech firms raised a total of $1.3 billion out of the total $5.3 billion in 2020 (24%)

Employee Lock-Up

But these key investors – often senior management of the firm – are also typically subject to a “lock-up” provision that requires them to place their shares in an escrow account after the IPO.

For companies qualifying for an IPO through the ‘asset test’ – which requires them to have A$4 million of net tangible assets or a market capitalisation of A$15 million as well as A$1.5 million of working capital – the ASX will usually oblige certain shareholders to place their shares in escrow for a period of 12 to 24 months, depending on the type of shareholder and other circumstances.6

The provision applies to shareholders like seed investors, promoters and major shareholders, related parties like directors and professionals or consultants who have been paid for their services in shares. It aims to prevent these early investors from selling – and potentially causing volatility – before the market has had time to properly value the company through trading.7

Pre-IPO employee investors are often counting down the months, weeks and days until they are allowed to sell stock.

For many of these early investors, though, the escrow period is a frustrating but necessary delay between wealth being created for them through the IPO and them having access to that wealth. Pre-IPO employee investors are often counting down the months, weeks and days until they are allowed to sell stock.

That does not mean they lack confidence in their company: usually it just means they have immediate opportunities, expenses or other capital needs. They may also need to fund a tax payment: the Australian Taxation Office treats employee stock options as income once they vest, which makes them subject to a tax rate of as much as 45%.

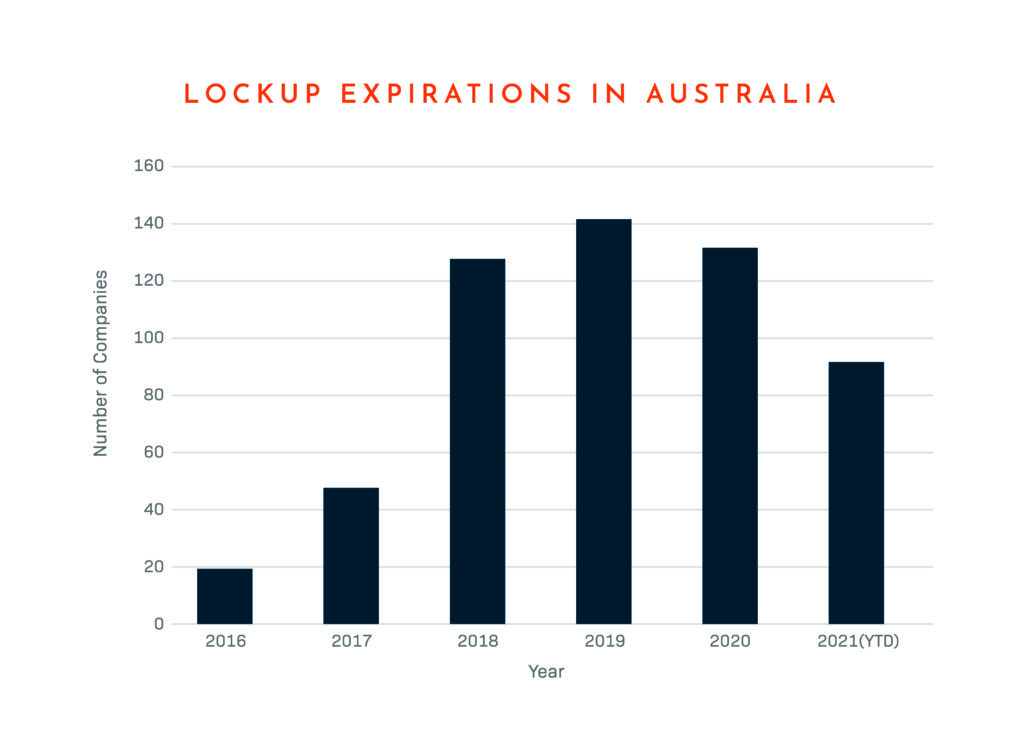

Number of companies in Australia with expiring lock ups from the year 2016 to 2021. The number of lockup expirations peaked in 2019.

Options for Equities Post Escrow

Investors in this situation sometimes assume that they have no alternative to selling their shares in order to meet their capital needs. Yet the private credit market does offer an attractive alternative: equity financing.

Through a non-recourse loan with EquitiesFirst, a shareholder can pledge a portion of their holding as collateral for their borrowing. The same number of shares will be returned to the borrower when the loan is repaid. During the life of the transaction, the original shareholder retains exposure to the performance of the shares and the right to receive dividend payments.

By accessing this alternative source of liquidity, a pre-IPO investor can retain their full shareholding when escrow ends, enjoy all the upside of owning the stock and make the investments, purchases or payments they had in mind.

إخلاء مسؤولية

أعدت هذه الوثيقة خصيصاً للمستثمرين المعتمدين أو المستثمرين المتطورين ماليًّا أو المستثمرين المحترفين أو المستثمرين المؤهلين، على النحو الذي يقتضيه القانون أو غيره، وهي ليست موجهة للأشخاص الذين لا يستوفون المتطلبات ذات الصلة وينبغي عدم استخدامها من أجلهم. يستخدم محتوى هذه الوثيقة لأغراض إعلامية فقط ويغلب عليه الطابع العام ولا يلبي أي غاية محددة أو حاجة مالية معينة. تخص وجهات النظر والآراء الواردة في هذه الوثيقة أطرافًا ثالثة ولا تعكس بالضرورة وجهات نظر شركة “إيكويتيز فيرست” أو آراءها. لم تفحص شركة “إيكويتيز فيرست” المعلومات الواردة في هذه الوثيقة أو لم تتحقق منها بشكل مستقل، ولا تقدم أي تعهد بمدى دقتها أو اكتمالها. تخضع الآراء والمعلومات الواردة في هذه الوثيقة للتغيير من دون إشعار. لا يمثل محتوى الوثيقة عرضًا لبيع (أو طلب عرض شراء) أي أوراق مالية أو استثمارات أو منتجات مالية (يشار إليها باسم “العرض”). يجب تقديم أي عرض مماثل لذلك فقط من خلال عرض ذي صلة أو وثائق أخرى تحدد شروطه وأحكامه المادية. لا يشكل أي محتوى وارد في هذه الوثيقة توصية أو طلبًا أو دعوة أو إغراء أو ترويجًا أو عرضًا لشراء أو بيع أي منتج استثماري من شركة “إيكويتيز فيرست” أو “إيكويتيز فيرست هولدينجز المحدودة” أو الشركات التابعة لها (يشار إليها مجتمعة باسم “إيكويتيز فيرست”)، ولا يجوز تفسير هذه الوثيقة بأي شكل من الأشكال على أنها مشورة استثمارية أو قانونية أو ضريبية أو توصية أو مرجع أو إقرار مقدم من شركة “إيكويتيز فيرست”. وعليك طلب المشورة المالية المستقلة قبل اتخاذ أي قرار استثماري بشأن منتج مالي معين.

تحتفظ هذه الوثيقة بحقوق الملكية الفكرية لشركة “إيكويتيز فيرست” في الولايات المتحدة ودول أخرى، ويشمل ذلك على سبيل المثال لا الحصر، الشعارات الخاصة بها وغيرها من العلامات التجارية وعلامات الخدمة المسجلة وغير المسجلة. تحتفظ الشركة بجميع الحقوق المتعلقة بملكيتها الفكرية الواردة في هذه الوثيقة. ينبغي لمستلمي هذه الوثيقة عدم توزيعها أو نشرها أو إعادة إنتاجها أو إتاحتها كليًّا أو جزئيًّا بأي شكل من الأشكال لأي شخص آخر، لا سيما الأشخاص في دولة قد يؤدي توزيع هذه الوثيقة فيها إلى خرق أي شرط قانوني أو تنظيمي.

لا تقدم شركة “إيكويتيز فيرست” أي تعهد أو ضمان فيما يتعلق بهذه الوثيقة، وتخلي مسؤوليتها صراحة عن أي ضمان ضمني بموجب القانون. وعليه تقر بأن شركة “إيكويتيز فيرست” ليست مسؤولة تحت أي ظرف من الظروف عن أي أضرار مباشرة أو غير مباشرة أو خاصة أو تبعية أو عرضية أو عقابية أيًّا كان نوعها، منها على سبيل المثال لا الحصر، أي أرباح مفقودة أو فرص ضائعة، حتى إذا تم إخطار الشركة بإمكانية وقوع مثل هذه الأضرار.

تدلي شركة “إيكويتيز فيرست” بالتصريحات الإضافية الآتية التي قد تطبق في دول الاختصاص القضائي المذكورة:

دبي: تخضع شركة “إيكويتيز فيرست هونج كونج المحدودة” (التي يشار إليها باسم “المكتب التمثيلي بمركز دبي المالي العالمي”) الكائنة في مبنى حي البوابة 4، الطابق 6، المكتب 7، مركز دبي المالي العالمي (التي تحمل ترخيصًا تجاريًّا رقم CL7354) للوائح سلطة دبي للخدمات المالية بصفتها مكتبًّا تمثيليًّا (رقم مرجع الشركة لدى سلطة دبي للخدمات المالية:F008752 ). جميع الحقوق محفوظة.

تُستخدم المواد الواردة في هذه الوثيقة لأغراض معلوماتية فقط وينبغي عدم تفسيرها على أنها مشورة مالية أو عرض أو طلب أو توصية لشراء منتجات مالية أو بيعها. تعد المعلومات الواردة في هذه الوثيقة عامة بطبيعتها، وأي مشورة واردة هنا هي عامة وقد تم إعدادها من دون النظر إلى أهدافك أو وضعك المالي أو ملاءمة منتجاتك المالية أو احتياجاتك. لذا قبل استخدام أي من هذه المعلومات، يجب أن تفكر في مدى ملاءمتها لأهدافك ووضعك المالي واحتياجاتك وطبيعة المنتج المالي ذي الصلة. يمكنك استشارة مستشار مالي معتمد إذا لم تكن بعض محتويات هذه الوثيقة واضحة بالنسبة إليك.

تختص هذه الوثيقة بمنتج مالي لا يخضع لأي شكل من أشكال التنظيم أو الاعتماد الخاص بسلطة دبي للخدمات المالية. لا تتحمل سلطة دبي للخدمات المالية أي مسؤولية عن مراجعة أي وثائق تتعلق بهذا المنتج المالي أو التحقق منها. وعليه، لم تعتمد سلطة دبي للخدمات المالية هذه الوثيقة أو أي وثائق أخرى مرتبطة بها ولم تتخذ أي خطوات للتحقق من المعلومات الواردة فيها، ولا تتحمل أي مسؤولية ناجمة عنها.

أستراليا: تحمل شركة “إيكويتيز فيرست هولدينجز (أستراليا) ذات المسؤولية المحدودة” (رقم الشركة في أستراليا: 399 644 142) ترخيصًا لمزاولة الخدمات المالية في أستراليا (رقم الترخيص: 387079). جميع الحقوق محفوظة.

توجه المعلومات الواردة في هذه الوثيقة للأشخاص في أستراليا فقط المصنفين بأنهم عملاء في قطاع التجارة بالجملة على النحو المحدد في القسم 761G من قانون الشركات لعام 2001. قد يُقيد توزيع المعلومات على الأشخاص الذين لا تنطبق عليهم هذه المعايير بموجب القانون، ويجب على الأشخاص الذين يمتلكونها طلب المشورة ومراعاة أي قيود تتعلق بها.

تستخدم المواد الواردة في هذه الوثيقة لأغراض معلوماتية فقط وينبغي عدم تفسيرها على أنها عرض أو طلب أو توصية لشراء منتجات مالية أو بيعها.

تُعد المعلومات الواردة في هذه الوثيقة عامة بطبيعتها وليست مشورة شخصية بشأن المنتجات المالية. أي مشورة واردة في الوثيقة هي عامة فقط وقد تم إعدادها من دون النظر إلى أهدافك أو وضعك المالي أو احتياجاتك. لذا قبل استخدام أي من هذه المعلومات، يجب أن تفكر في مدى ملاءمتها لأهدافك ووضعك المالي واحتياجاتك وطبيعة المنتج المالي ذي الصلة. عليك طلب المشورة المالية المستقلة وقراءة بيانات الإفصاح ذات الصلة أو وثائق العرض الأخرى قبل اتخاذ أي قرار استثماري بشأن منتج مالي معين.

التوقعات غير مضمونة، ولا ينبغي الاعتماد عليها بشكل مفرط. تعتمد هذه المعلومات على الآراء التي تتبناها شركة إكويتيز فيرست هولدينغز (أستراليا) ذات مسؤولية محدودة خاصة كما في تاريخ نشر هذا المحتوى

هونغ كونغ: تمتلك شركة “إيكويتيز فيرست هولدينجز هونج كونج المحدودة” ترخيصًا من النوع 1 من لجنة هونغ كونغ للأوراق المالية والعقود الآجلة، وهي مرخصة في هونغ كونغ بموجب قانون مقرضي الأموال (ترخيص مقرض الأموال رقم 2025/1493). لم تراجع لجنة هونغ كونغ للأوراق المالية والعقود الآجلة هذه الوثيقة. لا تمثل هذه الوثيقة عرضًا لبيع أوراق مالية أو طلبًا لشراء أي منتج تديره أو تقدمه شركة “إيكويتيز فيرست هولدينجز هونج كونج المحدودة”، لكنها موجهة للمستثمرين المحترفين لا للأفراد أو المؤسسات التي تكون هذه العروض أو الدعوات غير قانونية أو محظورة بالنسبة إليهم.

كوريا: توجه هذه الوثيقة فقط للمستهلكين الماليين المحترفين أو المستثمرين المحترفين أو المستثمرين المؤهلين الذين يتسلحون بالمعرفة ويتمتعون بالخبرة الكافية للدخول في معاملات تمويل الأوراق المالية، وهي غير مخصصة للأشخاص الذين لا يستوفون هذه المعايير وينبغي عدم استخدامهم إياها.