How equity-backed loans can meet the liquidity ambitions of Asia’s borrowers

Equity-backed lending is emerging as a compelling funding mechanism in the current environment, and it is worth examining its merits versus other liquidity options - particularly given the rapid growth in the number of potential borrowers in Asia this kind of lending could benefit.

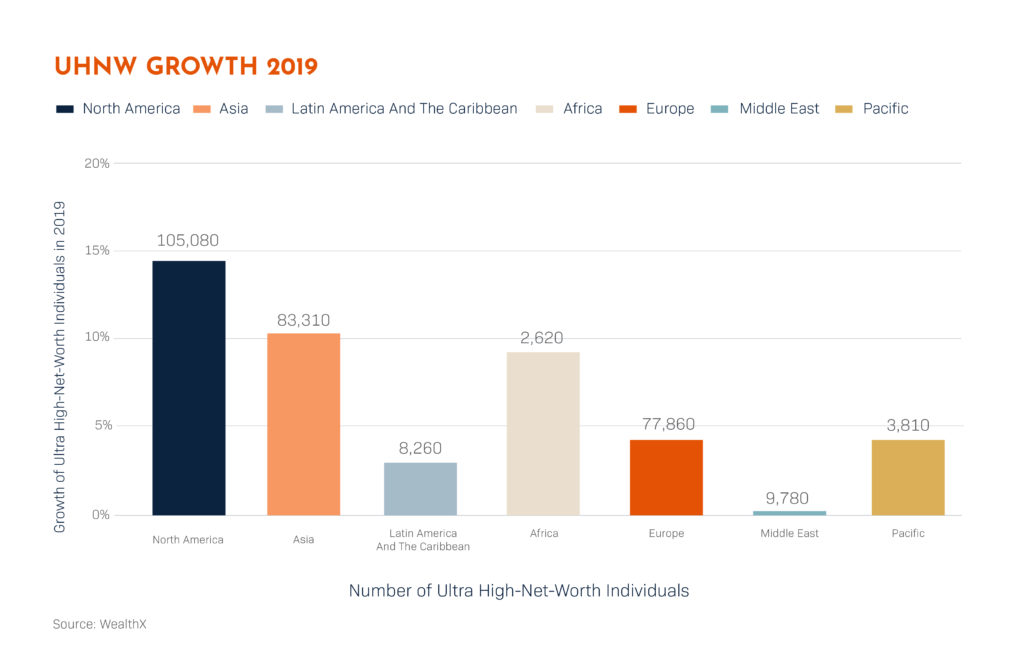

Asia’s ultra-high-net worth (UHNW) population – the second largest behind North America – grew 10.2% to 83,310 individuals in 2019.[1] As economic conditions, and consequent risks and opportunities, shift rapidly, many of these individuals will be looking for new ways to put their assets to work.

Asia 10.2% (83,310) North America 14.5% (105,080)

The premise is relatively simple: equity-backed loans allow investors, typically with concentrated holdings, to use their shares as collateral to unlock liquidity for other needs while still maintaining upside participation in the stock. At times their ambitions are business-oriented. The funds could be used to start a new venture, diversify investment or exercise options due to expire. Other projects are more personal – for example to address tax liabilities or to purchase “crown jewel” assets.

Through our two decades as a specialist in equities-backed lending, we have developed a unique approach that maximizes the potential of this model along two key dimensions - flexibility and efficiency.

Lending with agility

On a global basis, most of our loans average in the US$4 million range. Yet we can vary loan amounts considerably depending on borrower needs and market conditions. In markets such as Hong Kong with high liquidity and concentrations of wealth, the average loan size is many multiples larger. In Australia, the average loan size is just US$1 million, but transaction volume is high. In Europe, average deal sizes fall somewhere in the middle.

We are also able to structure liquidity solutions to the specific needs of each borrower by, for example, increasing or decreasing the tranche size, or adjusting the loan to value (LTV) ratio depending on their requirements.

Several borrowers have worked with us on repeat occasions due to this flexibility. For example, we have provided some borrowers a total of US$30 million in liquidity, but across six separate US$5 million tranches. Not surprisingly, we estimate up to 70% of our transactions are with repeat borrowers. Over the past five years, EquitiesFirst’s Asia offices have closed over $1 billion USD in loan transactions for UHNW individuals.

Value, delivered efficiently

The distinctive aspects of our business model also allow us to offer a quick and seamless experience to our borrowers. While we make sure that we conduct all necessary due diligence, we do not require extensive credit checks. The quality and value of the underlying asset – i.e. the equity the borrower supplies as collateral – mitigates the risk on our side of the transaction.

Interests are aligned during the term of the loan as the borrower’s equity is transferred to become a part of the EquitiesFirst portfolio and we become an investor in the stock alongside the owner. From then on, the borrower is simply required to pay a fixed interest rate - typically significantly lower than standard lending rates - on a quarterly basis; and at the end of the term, repay the loan. Once the principal is repaid, EquitiesFirst returns the same number of shares we received at initiation. This means the borrower retains all economic beneficial ownership, including value appreciation and dividend payments.

This level of efficiency is something that other capital providers, typically banks and other large financial institutions, are simply not in a position to offer. As equity-backed lending is typically a niche component of a large bank’s business at best, internal restrictions and a lack of focus limit their ability to act.

By contrast, as a dedicated equity-backed lender, we have worked for years to streamline and enhance our processes in a way that benefits the parties on both sides of each transaction. With a growing presence in Asia, we stand ready to bring these skills to bear as the region’s rising ranks of affluence seek new means to access the liquidity needed to achieve their goals.

أعدت هذه الوثيقة خصيصاً للمستثمرين المعتمدين أو المستثمرين المتطورين ماليًّا أو المستثمرين المحترفين أو المستثمرين المؤهلين، على النحو الذي يقتضيه القانون أو غيره، وهي ليست موجهة للأشخاص الذين لا يستوفون المتطلبات ذات الصلة وينبغي عدم استخدامها من أجلهم. يستخدم محتوى هذه الوثيقة لأغراض إعلامية فقط ويغلب عليه الطابع العام ولا يلبي أي غاية محددة أو حاجة مالية معينة. تخص وجهات النظر والآراء الواردة في هذه الوثيقة أطرافًا ثالثة ولا تعكس بالضرورة وجهات نظر شركة “إيكويتيز فيرست” أو آراءها. لم تفحص شركة “إيكويتيز فيرست” المعلومات الواردة في هذه الوثيقة أو لم تتحقق منها بشكل مستقل، ولا تقدم أي تعهد بمدى دقتها أو اكتمالها. تخضع الآراء والمعلومات الواردة في هذه الوثيقة للتغيير من دون إشعار. لا يمثل محتوى الوثيقة عرضًا لبيع (أو طلب عرض شراء) أي أوراق مالية أو استثمارات أو منتجات مالية (يشار إليها باسم “العرض”). يجب تقديم أي عرض مماثل لذلك فقط من خلال عرض ذي صلة أو وثائق أخرى تحدد شروطه وأحكامه المادية. لا يشكل أي محتوى وارد في هذه الوثيقة توصية أو طلبًا أو دعوة أو إغراء أو ترويجًا أو عرضًا لشراء أو بيع أي منتج استثماري من شركة “إيكويتيز فيرست” أو “إيكويتيز فيرست هولدينجز المحدودة” أو الشركات التابعة لها (يشار إليها مجتمعة باسم “إيكويتيز فيرست”)، ولا يجوز تفسير هذه الوثيقة بأي شكل من الأشكال على أنها مشورة استثمارية أو قانونية أو ضريبية أو توصية أو مرجع أو إقرار مقدم من شركة “إيكويتيز فيرست”. وعليك طلب المشورة المالية المستقلة قبل اتخاذ أي قرار استثماري بشأن منتج مالي معين.

تحتفظ هذه الوثيقة بحقوق الملكية الفكرية لشركة “إيكويتيز فيرست” في الولايات المتحدة ودول أخرى، ويشمل ذلك على سبيل المثال لا الحصر، الشعارات الخاصة بها وغيرها من العلامات التجارية وعلامات الخدمة المسجلة وغير المسجلة. تحتفظ الشركة بجميع الحقوق المتعلقة بملكيتها الفكرية الواردة في هذه الوثيقة. ينبغي لمستلمي هذه الوثيقة عدم توزيعها أو نشرها أو إعادة إنتاجها أو إتاحتها كليًّا أو جزئيًّا بأي شكل من الأشكال لأي شخص آخر، لا سيما الأشخاص في دولة قد يؤدي توزيع هذه الوثيقة فيها إلى خرق أي شرط قانوني أو تنظيمي.

لا تقدم شركة “إيكويتيز فيرست” أي تعهد أو ضمان فيما يتعلق بهذه الوثيقة، وتخلي مسؤوليتها صراحة عن أي ضمان ضمني بموجب القانون. وعليه تقر بأن شركة “إيكويتيز فيرست” ليست مسؤولة تحت أي ظرف من الظروف عن أي أضرار مباشرة أو غير مباشرة أو خاصة أو تبعية أو عرضية أو عقابية أيًّا كان نوعها، منها على سبيل المثال لا الحصر، أي أرباح مفقودة أو فرص ضائعة، حتى إذا تم إخطار الشركة بإمكانية وقوع مثل هذه الأضرار.

تدلي شركة “إيكويتيز فيرست” بالتصريحات الإضافية الآتية التي قد تطبق في دول الاختصاص القضائي المذكورة:

دبي: تخضع شركة “إيكويتيز فيرست هونج كونج المحدودة” (التي يشار إليها باسم “المكتب التمثيلي بمركز دبي المالي العالمي”) الكائنة في مبنى حي البوابة 4، الطابق 6، المكتب 7، مركز دبي المالي العالمي (التي تحمل ترخيصًا تجاريًّا رقم CL7354) للوائح سلطة دبي للخدمات المالية بصفتها مكتبًّا تمثيليًّا (رقم مرجع الشركة لدى سلطة دبي للخدمات المالية:F008752 ). جميع الحقوق محفوظة.

تُستخدم المواد الواردة في هذه الوثيقة لأغراض معلوماتية فقط وينبغي عدم تفسيرها على أنها مشورة مالية أو عرض أو طلب أو توصية لشراء منتجات مالية أو بيعها. تعد المعلومات الواردة في هذه الوثيقة عامة بطبيعتها، وأي مشورة واردة هنا هي عامة وقد تم إعدادها من دون النظر إلى أهدافك أو وضعك المالي أو ملاءمة منتجاتك المالية أو احتياجاتك. لذا قبل استخدام أي من هذه المعلومات، يجب أن تفكر في مدى ملاءمتها لأهدافك ووضعك المالي واحتياجاتك وطبيعة المنتج المالي ذي الصلة. يمكنك استشارة مستشار مالي معتمد إذا لم تكن بعض محتويات هذه الوثيقة واضحة بالنسبة إليك.

تختص هذه الوثيقة بمنتج مالي لا يخضع لأي شكل من أشكال التنظيم أو الاعتماد الخاص بسلطة دبي للخدمات المالية. لا تتحمل سلطة دبي للخدمات المالية أي مسؤولية عن مراجعة أي وثائق تتعلق بهذا المنتج المالي أو التحقق منها. وعليه، لم تعتمد سلطة دبي للخدمات المالية هذه الوثيقة أو أي وثائق أخرى مرتبطة بها ولم تتخذ أي خطوات للتحقق من المعلومات الواردة فيها، ولا تتحمل أي مسؤولية ناجمة عنها.

أستراليا: تحمل شركة “إيكويتيز فيرست هولدينجز (أستراليا) ذات المسؤولية المحدودة” (رقم الشركة في أستراليا: 399 644 142) ترخيصًا لمزاولة الخدمات المالية في أستراليا (رقم الترخيص: 387079). جميع الحقوق محفوظة.

توجه المعلومات الواردة في هذه الوثيقة للأشخاص في أستراليا فقط المصنفين بأنهم عملاء في قطاع التجارة بالجملة على النحو المحدد في القسم 761G من قانون الشركات لعام 2001. قد يُقيد توزيع المعلومات على الأشخاص الذين لا تنطبق عليهم هذه المعايير بموجب القانون، ويجب على الأشخاص الذين يمتلكونها طلب المشورة ومراعاة أي قيود تتعلق بها.

تستخدم المواد الواردة في هذه الوثيقة لأغراض معلوماتية فقط وينبغي عدم تفسيرها على أنها عرض أو طلب أو توصية لشراء منتجات مالية أو بيعها.

تُعد المعلومات الواردة في هذه الوثيقة عامة بطبيعتها وليست مشورة شخصية بشأن المنتجات المالية. أي مشورة واردة في الوثيقة هي عامة فقط وقد تم إعدادها من دون النظر إلى أهدافك أو وضعك المالي أو احتياجاتك. لذا قبل استخدام أي من هذه المعلومات، يجب أن تفكر في مدى ملاءمتها لأهدافك ووضعك المالي واحتياجاتك وطبيعة المنتج المالي ذي الصلة. عليك طلب المشورة المالية المستقلة وقراءة بيانات الإفصاح ذات الصلة أو وثائق العرض الأخرى قبل اتخاذ أي قرار استثماري بشأن منتج مالي معين.

التوقعات غير مضمونة، ولا ينبغي الاعتماد عليها بشكل مفرط. تعتمد هذه المعلومات على الآراء التي تتبناها شركة إكويتيز فيرست هولدينغز (أستراليا) ذات مسؤولية محدودة خاصة كما في تاريخ نشر هذا المحتوى

هونغ كونغ: تمتلك شركة “إيكويتيز فيرست هولدينجز هونج كونج المحدودة” ترخيصًا من النوع 1 من لجنة هونغ كونغ للأوراق المالية والعقود الآجلة، وهي مرخصة في هونغ كونغ بموجب قانون مقرضي الأموال (ترخيص مقرض الأموال رقم 2025/1493). لم تراجع لجنة هونغ كونغ للأوراق المالية والعقود الآجلة هذه الوثيقة. لا تمثل هذه الوثيقة عرضًا لبيع أوراق مالية أو طلبًا لشراء أي منتج تديره أو تقدمه شركة “إيكويتيز فيرست هولدينجز هونج كونج المحدودة”، لكنها موجهة للمستثمرين المحترفين لا للأفراد أو المؤسسات التي تكون هذه العروض أو الدعوات غير قانونية أو محظورة بالنسبة إليهم.

كوريا: توجه هذه الوثيقة فقط للمستهلكين الماليين المحترفين أو المستثمرين المحترفين أو المستثمرين المؤهلين الذين يتسلحون بالمعرفة ويتمتعون بالخبرة الكافية للدخول في معاملات تمويل الأوراق المالية، وهي غير مخصصة للأشخاص الذين لا يستوفون هذه المعايير وينبغي عدم استخدامهم إياها.