The advent of costly capital calls for a progressive solution

The market volatility that followed the abrupt end to a decade of ultra-low interest rates has made it clear that interest rates are a major driver of equity market performance. Having been forced to adjust their valuations and growth expectations over the past year, investors need to assess how a structurally higher cost of capital will affect their portfolio strategies in the longer term.

With US interest rates at their highest for 16 years after a rapid succession of hikes, the billion-dollar question for equity investors is how the battle against persistently high inflation will affect corporate earnings and economic growth around the world.

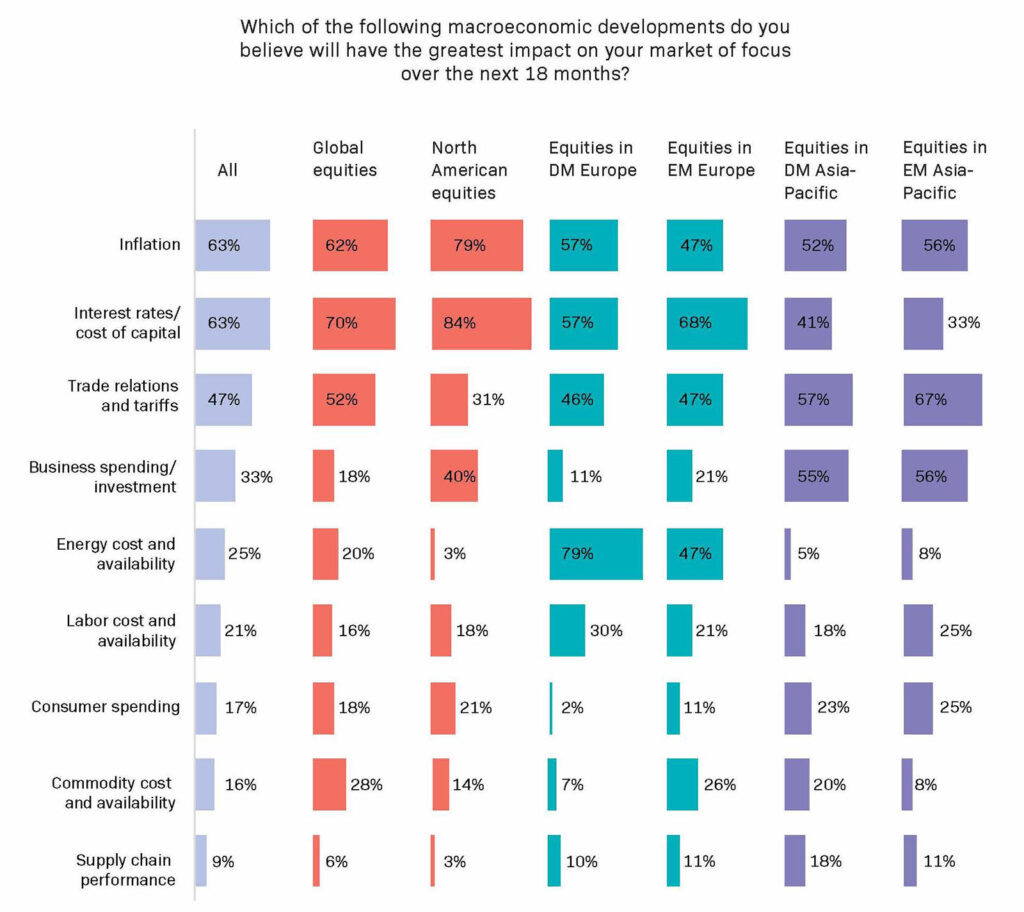

Nearly two-thirds of investors see inflation and interest rates as the macroeconomic factors with the greatest bearing on stock market performance over the next 18 months, according to a new study commissioned by EquitiesFirst and carried out by Institutional Investor. The general consensus is that rate rises are at or close to peaking, but there is certainly room for more surprises.

While markets are looking for cuts to support a slowing economy, policymakers in the US and Europe have warned that interest rates are likely to remain elevated until at least 2024, given that inflation is still well above their target range.[1]

The longer rates remain high, the more business and household borrowers will feel the squeeze from higher borrowing costs. This credit tightening has accelerated in recent months as lenders turn more cautious ahead of an expected recession and look to conserve their own liquidity. More than US$1.1 trillion of deposits have flowed out of US banks since the Fed began its hiking cycle in March 2022.[2]

Defaults on the rise

The EquitiesFirst study – which polled some 300 investment decision-makers across asset management firms, foundations, pension schemes and endowments – shows that the higher cost of capital is casting a cloud over investor sentiment.

Indeed, it could very well trigger the recession that the market has been predicting. Analysts at Deutsche Bank at the start of June argued that a wave of credit defaults is imminent, now that the combination of higher interest rates and tighter lending standards has put an end to a two-decade lending boom fueled by ultra-cheap money.[3] US high-yield bond defaults have risen to 2.1% from 1.1% last year, and loan defaults are up to 3.1% from 1.4% last year. The investment bank sees these peaking at 9% and 11.3%, respectively.[4]

When interest rates were close to zero, even financially stressed firms were able to raise debt and equity capital to continue operating. Now these companies – along with those that are relatively healthy but highly leveraged – may be unable to refinance maturing debt. Accordingly, the number of US businesses filing for bankruptcy is rising fast.[5]

The housing market, meanwhile, could be another casualty of the sharp rise in capital costs, with home prices tipped by some to fall as much as 10-15% this year.[6] Pricier mortgages mean not only that property owners may struggle to repay their debt but also have less disposable income to spend on other things.

All this could wreak havoc on financial markets, especially if leveraged positions need to be unwound quickly, giving investors plenty to think about for the rest of 2023.

Those who choose to stay invested in public markets are also facing higher margin costs and persistent volatility, while bargain-hunters will find it harder to access the capital they need to fund their purchases.

Tackling the capital crunch

With traditional lenders beating a hasty retreat, many borrowers are turning to private credit –financing from non-bank institutions such as asset managers or pension funds.

As investors have been increasing their allocations to private markets generally in recent years, private credit has become one of the fastest-growing asset classes. Private credit assets under management globally surged from US$342 billion in 2011 to US$1.4 trillion last year[7] and are expected to reach US$2.3 trillion by 2027.

Among the various forms of private credit, securities-backed financing is particularly well suited to today’s more volatile and uncertain market conditions. It typically offers lower borrowing costs than unsecured borrowing, and it is flexible, as virtually any asset – from stocks to cryptocurrencies to real estate – can serve as collateral for funding.

Although loans need to be structured carefully, in general risks are limited by the ability of lenders to recover their collateral, allowing them to offer highly competitive terms and rates.

EquitiesFirst has a 20-year track record in providing such financing – which we call ‘progressive capital’. As partners to long-term shareholders, we offer low-cost, flexible funding to help investors pursue new opportunities while maintaining the upside potential from their underlying holdings.

There are no clear answers to the big questions now facing equity investors, but there are clear opportunities for those who can act decisively in uncertain times and are willing to explore pioneering financing solutions.

أعدت هذه الوثيقة خصيصاً للمستثمرين المعتمدين أو المستثمرين المتطورين ماليًّا أو المستثمرين المحترفين أو المستثمرين المؤهلين، على النحو الذي يقتضيه القانون أو غيره، وهي ليست موجهة للأشخاص الذين لا يستوفون المتطلبات ذات الصلة وينبغي عدم استخدامها من أجلهم. يستخدم محتوى هذه الوثيقة لأغراض إعلامية فقط ويغلب عليه الطابع العام ولا يلبي أي غاية محددة أو حاجة مالية معينة. تخص وجهات النظر والآراء الواردة في هذه الوثيقة أطرافًا ثالثة ولا تعكس بالضرورة وجهات نظر شركة “إيكويتيز فيرست” أو آراءها. لم تفحص شركة “إيكويتيز فيرست” المعلومات الواردة في هذه الوثيقة أو لم تتحقق منها بشكل مستقل، ولا تقدم أي تعهد بمدى دقتها أو اكتمالها. تخضع الآراء والمعلومات الواردة في هذه الوثيقة للتغيير من دون إشعار. لا يمثل محتوى الوثيقة عرضًا لبيع (أو طلب عرض شراء) أي أوراق مالية أو استثمارات أو منتجات مالية (يشار إليها باسم “العرض”). يجب تقديم أي عرض مماثل لذلك فقط من خلال عرض ذي صلة أو وثائق أخرى تحدد شروطه وأحكامه المادية. لا يشكل أي محتوى وارد في هذه الوثيقة توصية أو طلبًا أو دعوة أو إغراء أو ترويجًا أو عرضًا لشراء أو بيع أي منتج استثماري من شركة “إيكويتيز فيرست” أو “إيكويتيز فيرست هولدينجز المحدودة” أو الشركات التابعة لها (يشار إليها مجتمعة باسم “إيكويتيز فيرست”)، ولا يجوز تفسير هذه الوثيقة بأي شكل من الأشكال على أنها مشورة استثمارية أو قانونية أو ضريبية أو توصية أو مرجع أو إقرار مقدم من شركة “إيكويتيز فيرست”. وعليك طلب المشورة المالية المستقلة قبل اتخاذ أي قرار استثماري بشأن منتج مالي معين.

تحتفظ هذه الوثيقة بحقوق الملكية الفكرية لشركة “إيكويتيز فيرست” في الولايات المتحدة ودول أخرى، ويشمل ذلك على سبيل المثال لا الحصر، الشعارات الخاصة بها وغيرها من العلامات التجارية وعلامات الخدمة المسجلة وغير المسجلة. تحتفظ الشركة بجميع الحقوق المتعلقة بملكيتها الفكرية الواردة في هذه الوثيقة. ينبغي لمستلمي هذه الوثيقة عدم توزيعها أو نشرها أو إعادة إنتاجها أو إتاحتها كليًّا أو جزئيًّا بأي شكل من الأشكال لأي شخص آخر، لا سيما الأشخاص في دولة قد يؤدي توزيع هذه الوثيقة فيها إلى خرق أي شرط قانوني أو تنظيمي.

لا تقدم شركة “إيكويتيز فيرست” أي تعهد أو ضمان فيما يتعلق بهذه الوثيقة، وتخلي مسؤوليتها صراحة عن أي ضمان ضمني بموجب القانون. وعليه تقر بأن شركة “إيكويتيز فيرست” ليست مسؤولة تحت أي ظرف من الظروف عن أي أضرار مباشرة أو غير مباشرة أو خاصة أو تبعية أو عرضية أو عقابية أيًّا كان نوعها، منها على سبيل المثال لا الحصر، أي أرباح مفقودة أو فرص ضائعة، حتى إذا تم إخطار الشركة بإمكانية وقوع مثل هذه الأضرار.

تدلي شركة “إيكويتيز فيرست” بالتصريحات الإضافية الآتية التي قد تطبق في دول الاختصاص القضائي المذكورة:

دبي: تخضع شركة “إيكويتيز فيرست هونج كونج المحدودة” (التي يشار إليها باسم “المكتب التمثيلي بمركز دبي المالي العالمي”) الكائنة في مبنى حي البوابة 4، الطابق 6، المكتب 7، مركز دبي المالي العالمي (التي تحمل ترخيصًا تجاريًّا رقم CL7354) للوائح سلطة دبي للخدمات المالية بصفتها مكتبًّا تمثيليًّا (رقم مرجع الشركة لدى سلطة دبي للخدمات المالية:F008752 ). جميع الحقوق محفوظة.

تُستخدم المواد الواردة في هذه الوثيقة لأغراض معلوماتية فقط وينبغي عدم تفسيرها على أنها مشورة مالية أو عرض أو طلب أو توصية لشراء منتجات مالية أو بيعها. تعد المعلومات الواردة في هذه الوثيقة عامة بطبيعتها، وأي مشورة واردة هنا هي عامة وقد تم إعدادها من دون النظر إلى أهدافك أو وضعك المالي أو ملاءمة منتجاتك المالية أو احتياجاتك. لذا قبل استخدام أي من هذه المعلومات، يجب أن تفكر في مدى ملاءمتها لأهدافك ووضعك المالي واحتياجاتك وطبيعة المنتج المالي ذي الصلة. يمكنك استشارة مستشار مالي معتمد إذا لم تكن بعض محتويات هذه الوثيقة واضحة بالنسبة إليك.

تختص هذه الوثيقة بمنتج مالي لا يخضع لأي شكل من أشكال التنظيم أو الاعتماد الخاص بسلطة دبي للخدمات المالية. لا تتحمل سلطة دبي للخدمات المالية أي مسؤولية عن مراجعة أي وثائق تتعلق بهذا المنتج المالي أو التحقق منها. وعليه، لم تعتمد سلطة دبي للخدمات المالية هذه الوثيقة أو أي وثائق أخرى مرتبطة بها ولم تتخذ أي خطوات للتحقق من المعلومات الواردة فيها، ولا تتحمل أي مسؤولية ناجمة عنها.

أستراليا: تحمل شركة “إيكويتيز فيرست هولدينجز (أستراليا) ذات المسؤولية المحدودة” (رقم الشركة في أستراليا: 399 644 142) ترخيصًا لمزاولة الخدمات المالية في أستراليا (رقم الترخيص: 387079). جميع الحقوق محفوظة.

توجه المعلومات الواردة في هذه الوثيقة للأشخاص في أستراليا فقط المصنفين بأنهم عملاء في قطاع التجارة بالجملة على النحو المحدد في القسم 761G من قانون الشركات لعام 2001. قد يُقيد توزيع المعلومات على الأشخاص الذين لا تنطبق عليهم هذه المعايير بموجب القانون، ويجب على الأشخاص الذين يمتلكونها طلب المشورة ومراعاة أي قيود تتعلق بها.

تستخدم المواد الواردة في هذه الوثيقة لأغراض معلوماتية فقط وينبغي عدم تفسيرها على أنها عرض أو طلب أو توصية لشراء منتجات مالية أو بيعها.

تُعد المعلومات الواردة في هذه الوثيقة عامة بطبيعتها وليست مشورة شخصية بشأن المنتجات المالية. أي مشورة واردة في الوثيقة هي عامة فقط وقد تم إعدادها من دون النظر إلى أهدافك أو وضعك المالي أو احتياجاتك. لذا قبل استخدام أي من هذه المعلومات، يجب أن تفكر في مدى ملاءمتها لأهدافك ووضعك المالي واحتياجاتك وطبيعة المنتج المالي ذي الصلة. عليك طلب المشورة المالية المستقلة وقراءة بيانات الإفصاح ذات الصلة أو وثائق العرض الأخرى قبل اتخاذ أي قرار استثماري بشأن منتج مالي معين.

التوقعات غير مضمونة، ولا ينبغي الاعتماد عليها بشكل مفرط. تعتمد هذه المعلومات على الآراء التي تتبناها شركة إكويتيز فيرست هولدينغز (أستراليا) ذات مسؤولية محدودة خاصة كما في تاريخ نشر هذا المحتوى

هونغ كونغ: تمتلك شركة “إيكويتيز فيرست هولدينجز هونج كونج المحدودة” ترخيصًا من النوع 1 من لجنة هونغ كونغ للأوراق المالية والعقود الآجلة، وهي مرخصة في هونغ كونغ بموجب قانون مقرضي الأموال (ترخيص مقرض الأموال رقم 2025/1493). لم تراجع لجنة هونغ كونغ للأوراق المالية والعقود الآجلة هذه الوثيقة. لا تمثل هذه الوثيقة عرضًا لبيع أوراق مالية أو طلبًا لشراء أي منتج تديره أو تقدمه شركة “إيكويتيز فيرست هولدينجز هونج كونج المحدودة”، لكنها موجهة للمستثمرين المحترفين لا للأفراد أو المؤسسات التي تكون هذه العروض أو الدعوات غير قانونية أو محظورة بالنسبة إليهم.

كوريا: توجه هذه الوثيقة فقط للمستهلكين الماليين المحترفين أو المستثمرين المحترفين أو المستثمرين المؤهلين الذين يتسلحون بالمعرفة ويتمتعون بالخبرة الكافية للدخول في معاملات تمويل الأوراق المالية، وهي غير مخصصة للأشخاص الذين لا يستوفون هذه المعايير وينبغي عدم استخدامهم إياها.