All things being equal, rising interest rates make currencies more attractive to investors, thereby causing exchange rates to rise. These forces have been on display in 2022, pushing the US dollar to multi-year highs against other major currencies. The dollar is also benefiting from its status as a safe haven at a time when the world is wracked by inflation and geopolitical stress, and major economies appear to be heading for a recession.

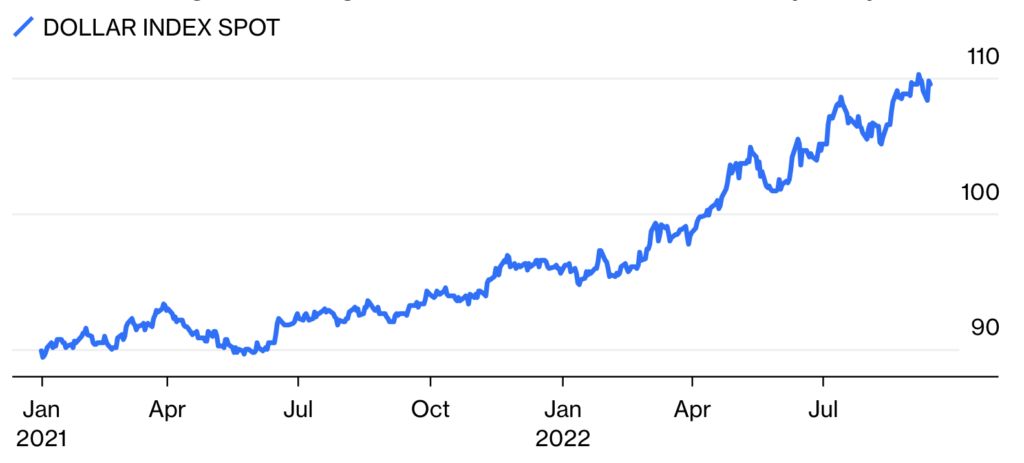

Admittedly, the dollar’s current run started from a relatively weak starting point. The greenback hit its lowest level in more than five years in May 2021, when markets still believed the US Federal Reserve (Fed) would keep its benchmark interest rate near zero for the foreseeable future.

But as inflation picked up, fuelling expectations that the Fed would begin raising rates — which it eventually did at a rapid clip starting in December 2021 — the dollar embarked on a steady ascent which has seen it breeze past 20-year highs against the euro, yen and pound sterling this year.

The strength of the US dollar in the face of a decidedly gloomy global economic outlook underscores its status as the world’s dominant reserve currency. It also highlights how far the Fed’s policy decisions can reverberate around the world. Right now, the Fed’s determination to tame inflation at home is causing widespread pain abroad, as well as hurting US exports and reducing profits earned overseas by US companies in dollar terms.

Heavy is the crown of dollar dominance

The dollar’s strength comes from its function as the world’s reserve currency and the unit of exchange for most global commodities and a big chunk of global trade. According to a study carried out by the International Monetary Fund, an estimated 40% of the world’s trade deals are carried out in dollars.[1]

Energy and food commodity prices have already risen sharply this year as a result of supply shocks that were exacerbated and prolonged by the Russia-Ukraine war. But countries whose currencies have declined against the dollar face even steeper bills. They also must contend with ballooning payments on their US dollar-denominated debt.

For many emerging market economies, the higher cost of dollar borrowing negates the benefits of the export boost they get from having a weaker currency.[2] And exporters in many developed nations are also unable to take full competitive advantage of a favorable exchange rate because their output is constrained by energy disruptions.

The trade-weighted average of the dollar has risen relentlessly this year

In short, beyond American travelers benefiting from cheaper holidays abroad, there are few unequivocal winners from the strong dollar or the interest rate hikes driving it. In the past 40 years, rapidly rising US rates have been one of the primary triggers of international financial instability and are now being viewed as a major threat to the global economy as other central banks are forced to raise their own rates to defend their currencies.[3]

How can investors respond?

Currency hedging or investing in funds that maintain constant hedges is one strategy, which, while not necessarily a means of outperforming, does help minimise volatility.

Alternatively, some suggest that the dollar may have overshot, creating an attractive buying opportunity in international holdings — though that must be weighed against the risk from higher dollar-denominated debt repayment burdens.[4] Valuations are also an important metric to think about: there is now more value in value stocks than in any other cycle since 1990.[5]

Pursuing any of these strategies has become more challenging in light of tightening liquidity conditions. Securities-backed financing provides an attractive solution to access liquidity when capital is in short supply. It provides a source of funding investors can use to diversify their positions to other geographies and sectors or obtain currency hedges. Importantly, they can do so without sacrificing the upside potential of their core holdings, which they can keep hold of and only consider selling once liquidity conditions improve.

When might the dollar weaken?

The dollar could lose steam once the US decides inflation is under control and eases off the monetary brakes – something it has ruled out until at least the end of 2022. Atlanta Fed President Raphael Bostic suggested rate hikes might be paused once the policy rate reaches between 4% and 4.5% by December.[6] Given that inflation, employment and business activity in the US are all stronger than in other major economies in Europe and Asia, that gap also needs to narrow for the dollar to weaken. And because the US is a net energy exporter, a tempering of global energy prices would also help rein in its currency.[7]

Investors need to closely watch these signs, but trying to accurately predict currency markets can often be a fruitless endeavor for even the most seasoned currency experts. With access to a flexible source of capital, investors can remain nimble and rebalance their portfolios in response to the dollar’s ebb and flow.

Past performance does not guarantee future returns, and individual returns are not guaranteed or warranted.

This Document is intended solely for accredited investors, sophisticated investors, professional investors, or otherwise qualified investors, as may be required by law or otherwise, and it is not intended for, and should not be used by, persons who do not meet the relevant requirements. The content provided herein is for informational purposes only and is general in nature and not targeted to any specific objective or financial need. The views and opinions expressed in this Document have been prepared by third parties and do not necessarily reflect the views and opinions of EquitiesFirst. EquitiesFirst has not independently examined or verified the information provided herein, and no representation is made that it is accurate or complete. Opinions and information herein are subject to change without notice. The content provided does not constitute an offer to sell (or solicitation of an offer to purchase) any securities, investments, or any financial products (“Offer”). Any such Offer shall only be made through a relevant offering or other documentation which sets forth its material terms and conditions. Nothing contained in this Document shall constitute a recommendation, solicitation, invitation, inducement, promotion, or offer for the purchase or sale of any investment product by Equities First Holdings, LLC or its subsidiaries (collectively, “EquitiesFirst”), nor shall this Document be construed in any way as investment, legal, or tax advice, or as a recommendation, reference, or endorsement by EquitiesFirst. You should seek independent financial advice prior to making an investment decision about a financial product.

This Document contains the intellectual property of EquitiesFirst in the United States and other countries, including, without limitation, their respective logos and other registered and unregistered trademarks and service marks. EquitiesFirst reserves all rights in and to their intellectual property contained in this Document. The Document should not be distributed, published, reproduced or otherwise made available in whole or in part by recipients to any other person and, in particular, should not be distributed to persons in any country where such distribution may lead to a breach of any legal or regulatory requirement.

EquitiesFirst make no representation or warranty with respect to this Document and expressly disclaim any implied warranty under law. You acknowledge that EquitiesFirst is not liable under any circumstances for any direct, indirect, special, consequential, incidental, or punitive damages whatsoever, including, without limitation, any lost profits or lost opportunity, even if EquitiesFirst has been advised of the possibility of such damages.

EquitiesFirst makes the following further statements that may be applicable in the stated jurisdiction:

Australia: Equities First Holdings (Australia) Pty Ltd (ACN: 142 644 399) holds an Australian Financial Services Licence (AFSL Number: 387079). All rights reserved.

The information contained on this Document is intended for persons located in Australia only and classified as a Wholesale Client only as defined in Section 761G of the Corporations Act 2001. The distribution of information to persons outside this criteria may be restricted by law and persons who come into possession of it should seek advice and observe any such restriction.

The material contained in this Document is for information purposes only and should not be construed as an offer or solicitation or recommendation to buy or sell financial products.

The information contained in this Document is intended to be general in nature and is not personal financial product advice. Any advice contained in the Document is general advice only and has been prepared without considering your objectives, financial situation or needs. Before acting on any information, you should consider the appropriateness of the information provided and the nature of the relevant financial product having regard to your objectives, financial situation and needs. You should seek independent financial advice and read the relevant disclosure statements or other offer documents prior to making an investment decision about a financial product.

Forecasts are not guaranteed, and undue reliance should not be placed on them. This information is based on views held by Equities First Holdings (Australia) Pty Ltd as at the publishing date of this material.

Dubai: Equities First Holdings Hong Kong Ltd (DIFC Representative Office) at Gate Precinct Building 4, 6th Floor, Office 7, Dubai International Financial Centre (commercial license number CL7354) is regulated by the Dubai Financial Services Authority (“DFSA”) as a Representative Office (DFSA Firm Reference No.: F008752). All rights reserved.

The information contained in this document is intended to be general in nature, and, to the extent that it is perceived as advice, any advice contained in this document is general advice only and has been prepared without considering your objectives, financial situation, suitability of the financial products or your needs.

The material contained in this document is for information purposes only and should not be construed as financial advice, including an offer or solicitation or recommendation to buy or sell financial products. The information contained in this document is intended to be general in nature and any advice contained in this document is general advice only and has been prepared without considering your objectives, financial situation, suitability of the financial products or your needs. Before acting on any information, you should consider the appropriateness of the information provided and the nature of the relevant financial product having regard to your objectives, financial situation and needs. If you do not understand the contents of this document, you should consult an authorised financial adviser.

This document relates to a financial product which is not subject to any form of regulation or approval by the DFSA. The DFSA has no responsibility for reviewing or verifying any documents in connection with this financial product. Accordingly, the DFSA has not approved this document or any other associated documents nor taken any steps to verify the information set out in this document, and has no responsibility for it.

Hong Kong: Equities First Holdings Hong Kong Limited is licensed under the Money Lenders Ordinance (Money Lender’s Licence No. 1659/2024) and to carry on the business of dealing in securities (Type 1 licence) under the Securities and Futures Ordinance (“SFO”) (CE No. BFJ407). This Document has not been reviewed by the Hong Kong Securities and Futures Commission. It is not intended as an offer to sell securities or a solicitation to buy any product managed or provided by Equities First Holdings Hong Kong Limited and is only intended for persons who qualify as Professional Investors under the SFO. This document is not directed to individuals or organizations for whom such offers or invitations would be unlawful or prohibited.

Korea: The foregoing is intended solely for sophisticated investors, professional investors or otherwise qualified investors who have sufficient knowledge and experience in entering into securities financing transactions. It is not intended for, and should not be used by, persons who do not meet those criteria.

United Kingdom: Equities First (London) Limited is authorised and regulated in the UK by the Financial Conduct Authority (“FCA”). In the UK, this Document is only being distributed and made available to persons of the kind described in Article 19(5) (investment professionals) and Article 49(2) (high net worth companies, unincorporated associations etc.) of Part IV of the Financial Services and Markets Act 2000 (Financial Promotion) Order 2005 (‘’FPO’’) and any investment activity to which this presentation relates is only available to, and will only be engaged in with, such persons. Persons who do not have professional experience in matters relating to investment or who are not persons to whom Article 49 of the FPO applies should not rely on this document. This Document is only prepared for and available to persons who qualify as Professional Investors under the Markets in Financial Instruments Directive.