Please read the following Disclaimer and click "Proceed To Website" to continue. Thank you.

IMPORTANT INFORMATION ABOUT ACCESS TO THIS WEBSITE

www.equitiesfirst.com/uk (website) and any information contained therein (i) is only intended for persons classified as Professional Clients and Eligible Counterparties for the purposes of FCA Rules and (ii) should only be accessed by persons located in a jurisdiction or country where access to such information is not contrary to local law and regulation.

Information on this website must not be relied or acted upon by any other persons.

The investments and investment services referred to on this website may not be suitable for all investors. If in doubt investors should seek professional, independent financial advice, including the tax consequences in respect of any proposed course of action, before making any investment decision.

The information contained in this website does not constitute an offer or solicitation in any jurisdiction in which it is not authorised, or to any person to whom such offer or solicitation is unlawful.

All persons accessing this website do so on an unsolicited basis and on their own initiative. It is the responsibility of persons accessing this website to inform themselves of, and act in accordance with, the legal and regulatory requirements in their jurisdiction of citizenship, residence or domicile.

This website should not be regarded as an offer or solicitation, or recommendation to conduct investment business, as defined by the Financial Services and Markets Act 2000, in any jurisdiction other than the United Kingdom.

This website is for residents of the United Kingdom only. If you are not resident in the United Kingdom you must not view this website.

Investors who are resident in or are citizens of any country other than the United Kingdom may be subject to local restrictions, therefore, the information contained in this website is not for distribution outside the United Kingdom. Under no circumstances should information or any part of it be copied, reproduced or redistributed.

Equities First (London) Limited and its affiliates disclaim all responsibility if persons access the Website, or the information on it, contrary to such legal and regulatory requirements.

If you have any doubts about your status, you must not access this website.

Please contact Equities First (London) Limited if you require any further information on your status. Definitions of 'professional client' and 'eligible counterparty' can be found in the Glossary of the FCA Handbook which can be accessed here.

Please read the Terms & Conditions of Use below carefully. These set out the terms and conditions for accessing this Website. After you have read and understood the Terms & Conditions of Use, you may click "Proceed To Website" to proceed. By doing so, you:

(i) Confirm that you are permitted to access this Website because you are a professional client or an eligible counterparty for the purposes of the FCA Rules.

(ii) Confirm that you are accessing this Website on an unsolicited basis, on your own initiative and in compliance with the laws and regulations of the jurisdiction or country in which you are residing.

(iii) Acknowledge expressly that you have read and understood the Terms & Conditions of Use and agree to abide by them.

To proceed, you must also agree to meet all Terms and Conditions set forth by Equities First (London) Limited as outlined here.

If you do not agree with these Terms and Conditions of Use and/or you are a retail client for the purposes of the FCA Rules, you are not permitted to access this Website.

Given the uncertainty around inflation, interest rates and energy prices, as well as geopolitical concerns related to the war in Ukraine, the one thing investors broadly agree on is that equity markets are bound to remain volatile.

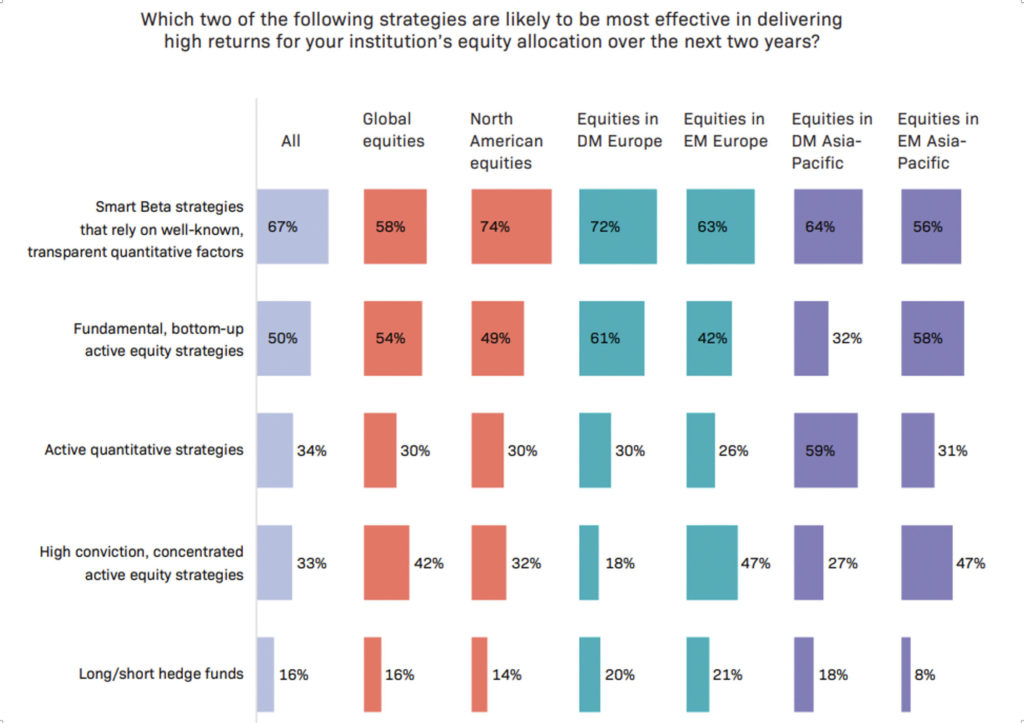

There is, however, a broad consensus on the most effective way to invest. In a landmark study by EquitiesFirst in conjunction with Institutional Investor, smart beta strategies came out ahead when investment decision-makers at global financial institutions were asked to rank the two investment strategies they believed would deliver high returns over the next two years. Smart beta investing was especially favored by investors focused on the world’s most liquid and developed equity markets, while those involved in developing markets showed a preference for fundamental, bottom-up active strategies.

Smart beta investing is essentially an alternative way to take passive exposure in markets by applying some of the factors rules used in active management – such as value, momentum, low-volatility and quality – to fine-tune broad index strategies. Investors generally see smart beta investing as a way to complement or tactically enhance overall performance within a diversified portfolio, at a lower cost compared to actively managed strategies.

The factor weightings applied to smart beta funds can be revised as market conditions evolve, meaning there is scope for more frequent rebalancing than with traditional index funds.[1]

As such, smart beta ETFs are sometimes described as “quasi-active.” Though this tends to give them slightly higher expense ratios than market cap-based passive benchmark index products, their fees are still considerably lower than those of actively managed funds.

The balance has tipped

Last year marked a milestone in the gradual shift away from actively managed equity funds, with assets under management in passive funds surpassing active funds for the first time.[2] Smart beta ETFs constitute a steadily expanding share of the passive investing universe, accounting for just over 16% of all ETF assets under management (AUM) in the US at the end of 2022.[3] At current growth rates, they are projected to reach US$1 trillion in AUM by the end of 2023.

In addition to being well suited to current market conditions, smart beta strategies are clearly also in vogue because of their recent strong performance, having delivered returns as high as 15%[4] last year even as major markets fell by around 20%. Among these, multi-factor ETFs – as opposed to those managed with a single factor weighting – were considered the “hot ticket.”

Not best for all markets

Still, smart beta ETFs may not be the best way to access all types of markets. According to the survey data and interviews from theEquitiesFirst x Institutional Investor study, they are best suited to the developed markets of North America, Europe, and Asia-Pacific – as opposed to developing and emerging ones – due largely to their efficiency and robust trading volumes.

Investors focused on North America, for example, noted that it was rare for active stock picking strategies to outperform in local markets. Portfolio managers focused on such developed markets over the past decade have tended to invest the bulk of their capital passively in large-cap equities to keep up with the relevant benchmarks, while taking smaller positions in small caps and emerging markets to seek alpha at the periphery.

By contrast, in emerging markets, which are generally characterized by inefficiencies, skilled managers can reliably outperform the broader market.

In the higher risk/return markets of developing Europe and Asia-Pacific, where information for investment decision making is at times uneven and trading volume is thin, the study found that concentrated high-conviction strategies are more likely to be viewed as highly effective.

More broadly, the study reveals that institutional investors value diversification and index-based strategies as the foundations of any equities portfolio. Individual investors can adopt a similar approach through smart beta funds.

With 1,275 different smart beta ETFs listed globally on 48 exchanges in 38 countries,[5] there is certainly no shortage of choice. Investors should pay heed to the key differences among them. They must assess the merits and current relevance of the indices, biases and specific factors used by each strategy. They should also consider which firm constitutes the underlying index and which sponsors the ETF.

Having determined which smart beta ETFs are right for them, investors can turn to securities-backed financing to access liquidity to acquire them. Using their equity or crypto as collateral, they can secure a flexible, cost-effective and stable source of capital, with which they can maneuver deftly into new positions and strategies without sacrificing upside from their underlying holdings.

With volatility likely to remain a feature of the global equity markets for the foreseeable future, it is hard for equity investors to know where to turn. The survey of institutional investors suggests that smart beta strategies are worth a closer look.

Past performance does not guarantee future returns, and individual returns are not guaranteed or warranted.

This Document is intended solely for accredited investors, sophisticated investors, professional investors, or otherwise qualified investors, as may be required by law or otherwise, and it is not intended for, and should not be used by, persons who do not meet the relevant requirements. The content provided herein is for informational purposes only and is general in nature and not targeted to any specific objective or financial need. The views and opinions expressed in this Document have been prepared by third parties and do not necessarily reflect the views and opinions of EquitiesFirst. EquitiesFirst has not independently examined or verified the information provided herein, and no representation is made that it is accurate or complete. Opinions and information herein are subject to change without notice. The content provided does not constitute an offer to sell (or solicitation of an offer to purchase) any securities, investments, or any financial products (“Offer”). Any such Offer shall only be made through a relevant offering or other documentation which sets forth its material terms and conditions. Nothing contained in this Document shall constitute a recommendation, solicitation, invitation, inducement, promotion, or offer for the purchase or sale of any investment product by Equities First Holdings, LLC or its subsidiaries (collectively, “EquitiesFirst”), nor shall this Document be construed in any way as investment, legal, or tax advice, or as a recommendation, reference, or endorsement by EquitiesFirst. You should seek independent financial advice prior to making an investment decision about a financial product.

This Document contains the intellectual property of EquitiesFirst in the United States and other countries, including, without limitation, their respective logos and other registered and unregistered trademarks and service marks. EquitiesFirst reserves all rights in and to their intellectual property contained in this Document. The Document should not be distributed, published, reproduced or otherwise made available in whole or in part by recipients to any other person and, in particular, should not be distributed to persons in any country where such distribution may lead to a breach of any legal or regulatory requirement.

EquitiesFirst make no representation or warranty with respect to this Document and expressly disclaim any implied warranty under law. You acknowledge that EquitiesFirst is not liable under any circumstances for any direct, indirect, special, consequential, incidental, or punitive damages whatsoever, including, without limitation, any lost profits or lost opportunity, even if EquitiesFirst has been advised of the possibility of such damages.

EquitiesFirst makes the following further statements that may be applicable in the stated jurisdiction:

Australia: Equities First Holdings (Australia) Pty Ltd (ACN: 142 644 399) holds an Australian Financial Services Licence (AFSL Number: 387079). All rights reserved.

The information contained on this Document is intended for persons located in Australia only and classified as a Wholesale Client only as defined in Section 761G of the Corporations Act 2001. The distribution of information to persons outside this criteria may be restricted by law and persons who come into possession of it should seek advice and observe any such restriction.

The material contained in this Document is for information purposes only and should not be construed as an offer or solicitation or recommendation to buy or sell financial products.

The information contained in this Document is intended to be general in nature and is not personal financial product advice. Any advice contained in the Document is general advice only and has been prepared without considering your objectives, financial situation or needs. Before acting on any information, you should consider the appropriateness of the information provided and the nature of the relevant financial product having regard to your objectives, financial situation and needs. You should seek independent financial advice and read the relevant disclosure statements or other offer documents prior to making an investment decision about a financial product.

Forecasts are not guaranteed, and undue reliance should not be placed on them. This information is based on views held by Equities First Holdings (Australia) Pty Ltd as at the publishing date of this material.

Dubai: Equities First Holdings Hong Kong Ltd (DIFC Representative Office) at Gate Precinct Building 4, 6th Floor, Office 7, Dubai International Financial Centre (commercial license number CL7354) is regulated by the Dubai Financial Services Authority (“DFSA”) as a Representative Office (DFSA Firm Reference No.: F008752). All rights reserved.

The material contained in this document is for information purposes only and should not be construed as financial advice, including an offer or solicitation or recommendation to buy or sell financial products. The information contained in this document is intended to be general in nature and any advice contained in this document is general advice only and has been prepared without considering your objectives, financial situation, suitability of the financial products or your needs. Before acting on any information, you should consider the appropriateness of the information provided and the nature of the relevant financial product having regard to your objectives, financial situation and needs. If you do not understand the contents of this document, you should consult an authorised financial adviser.

This document relates to a financial product which is not subject to any form of regulation or approval by the DFSA. The DFSA has no responsibility for reviewing or verifying any documents in connection with this financial product. Accordingly, the DFSA has not approved this document or any other associated documents nor taken any steps to verify the information set out in this document, and has no responsibility for it.

Hong Kong: Equities First Holdings Hong Kong Limited is licensed under the Money Lenders Ordinance (Money Lender’s Licence No. 1493/2025) and to carry on the business of dealing in securities (Type 1 licence) under the Securities and Futures Ordinance (“SFO”) (CE No. BFJ407). This Document has not been reviewed by the Hong Kong Securities and Futures Commission. It is not intended as an offer to sell securities or a solicitation to buy any product managed or provided by Equities First Holdings Hong Kong Limited and is only intended for persons who qualify as Professional Investors under the SFO. This document is not directed to individuals or organizations for whom such offers or invitations would be unlawful or prohibited.

Korea: The foregoing is intended solely for sophisticated investors, professional investors or otherwise qualified investors who have sufficient knowledge and experience in entering into securities financing transactions. It is not intended for, and should not be used by, persons who do not meet those criteria.

United Kingdom: Equities First (London) Limited is authorised and regulated in the UK by the Financial Conduct Authority (“FCA”). In the UK, this Document is only being distributed and made available to persons of the kind described in Article 19(5) (investment professionals) and Article 49(2) (high net worth companies, unincorporated associations etc.) of Part IV of the Financial Services and Markets Act 2000 (Financial Promotion) Order 2005 (‘’FPO’’) and any investment activity to which this presentation relates is only available to, and will only be engaged in with, such persons. Persons who do not have professional experience in matters relating to investment or who are not persons to whom Article 49 of the FPO applies should not rely on this document. This Document is only prepared for and available to persons who qualify as Professional Investors under the Markets in Financial Instruments Directive.