Assessing the untapped potential of equity-backed lending in Asia’s high-growth markets

Global banks have made significant inroads in the region. However, we would argue that Asia’s potential in the private credit space is still far from being fully realized on multiple fronts.

According to recent Bloomberg figures, the global private credit market is worth an estimated US$800 billion. [1] Asia is a disproportionately small slice of that pie. In fact, by some estimates, Asia Pacific receives less than 10% of capital allocation to private credit strategies, even though the region delivers around one-third of global GDP. [2] This mismatch signals substantial untapped demand in view of the region’s long-term growth trajectory.

The rapid evolution of Greater China and other Asian economies, and rise of the region’s markets, offer huge opportunities for equity-backed lending, a versatile and innovative form of private credit in which owners of liquid stocks employ these assets as collateral to access capital.

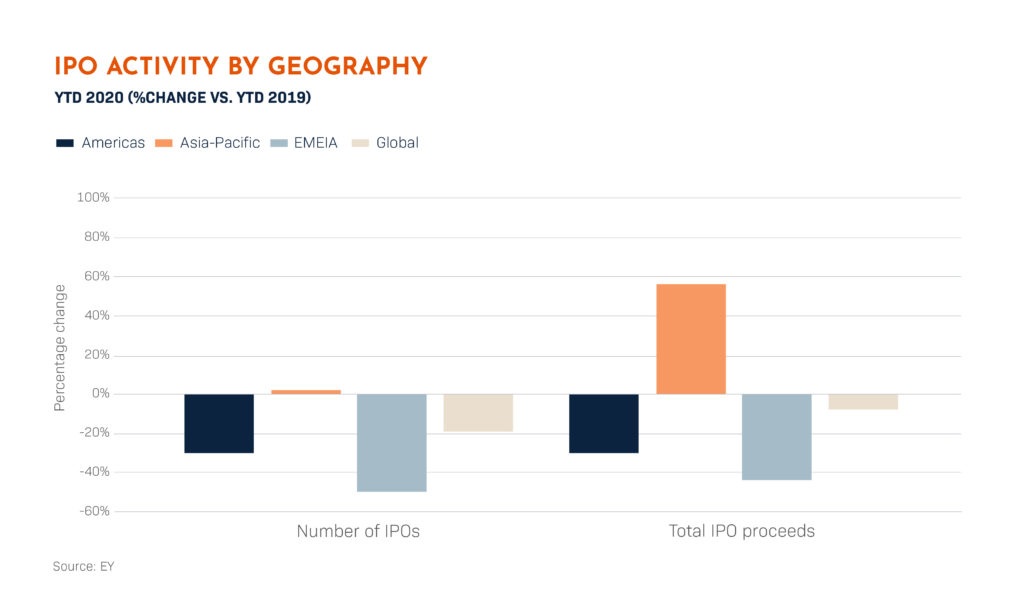

Asia Pacific stock markets have remained relatively robust engines of progress and prosperity even among the havoc that Covid-19 has brought to markets worldwide. One indicator of their vibrancy is the surge in IPO activity. In the first half of 2020, share listings in Greater China jumped 29% from the same period last year, and the amount of money that was raised rose 72%. The Hong Kong and Shanghai exchanges led the charge – underscoring the resilience of these two financial hubs. [3]

Benchmarks in South Korea, Japan and Taiwan have managed to post healthy gains over the last year despite at times volatile conditions. [4] Markets have been supported by both abundant liquidity and strong appetite from investors within in the region. Hong Kong’s market, for example, saw record inflows over the first quarter from the Connect scheme providing access to mainland Chinese investors. [5]

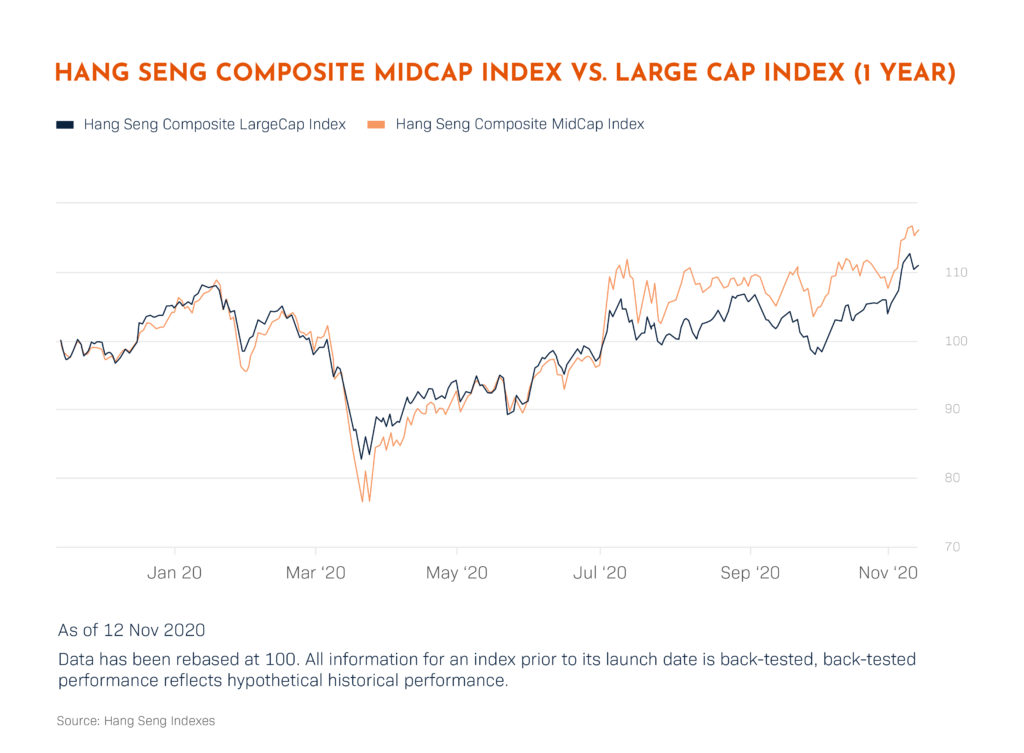

Interestingly, while the region has no shortage of corporate superstars, there are many indications lesser-known - but no less dynamic - mid-cap firms are where a lot of growth potential and investor interest are concentrated. For much of 2020, Tokyo’s Nikkei 225 benchmark has been roundly outperformed by the Nikkei 500, [6] a broader pool of more new economy and services-focused enterprises. Similarly, in Hong Kong the Hang Seng Composite MidCap Index produced around double the returns of its large cap counterpart. [7]

Investing in the region’s future

All this points to a growing and diverse network of regional investors who hold an expanding pool of high-potential assets, but can access only a limited range of funding opportunities. It is exactly this gap that equity-backed lending is designed to address.

We have identified chronically underserved borrower segments, especially in places like Hong Kong and South Korea, where investors and UHNWIs are keen to obtain funds for a range of purposes, from bolstering family businesses to diversifying investments. Yet, global banks are not positioned to offer effective solutions, and these investors are often unaware there is a sustainable means for them to access funding based on their equity portfolios.

This is why, after 20 years in this highly specialised sector, we now find ourselves registering the largest volume of new business among asset owners in Hong Kong, mainland China and South Korea. These markets continue to provide a healthy pipeline of transactions as the demand for liquidity – and financial security – increases.

This dynamism is precisely why EquitiesFirst is committed to investing further in our Asia operations. Our core Asia markets include China (Hong Kong), South Korea, Singapore and Thailand. We now have six offices in the region, most recently expanding our onshore China presence with offices in Beijing and Shanghai. The unique elements of our approach to equity-backed lending, which carefully balances the interests of lender and borrower, makes bricks-and-mortar presence key to engaging with each market and building long-term local partnerships.While other forms of funding will always have their place, our expertise and long-term approach to lending against equity allows us to be flexible and constructive on a broader population of assets. Listed shares with lower liquidity and higher volatility are difficult for banks to manage via traditional margin loans, but we understand that underlying these shares are often robust and sustainable businesses. By partnering and aligning interests with key shareholders, we see a tremendous opportunity to be a part of Asia’s growth story and the development of the regional private credit market.

أعدت هذه الوثيقة خصيصاً للمستثمرين المعتمدين أو المستثمرين المتطورين ماليًّا أو المستثمرين المحترفين أو المستثمرين المؤهلين، على النحو الذي يقتضيه القانون أو غيره، وهي ليست موجهة للأشخاص الذين لا يستوفون المتطلبات ذات الصلة وينبغي عدم استخدامها من أجلهم. يستخدم محتوى هذه الوثيقة لأغراض إعلامية فقط ويغلب عليه الطابع العام ولا يلبي أي غاية محددة أو حاجة مالية معينة. تخص وجهات النظر والآراء الواردة في هذه الوثيقة أطرافًا ثالثة ولا تعكس بالضرورة وجهات نظر شركة “إيكويتيز فيرست” أو آراءها. لم تفحص شركة “إيكويتيز فيرست” المعلومات الواردة في هذه الوثيقة أو لم تتحقق منها بشكل مستقل، ولا تقدم أي تعهد بمدى دقتها أو اكتمالها. تخضع الآراء والمعلومات الواردة في هذه الوثيقة للتغيير من دون إشعار. لا يمثل محتوى الوثيقة عرضًا لبيع (أو طلب عرض شراء) أي أوراق مالية أو استثمارات أو منتجات مالية (يشار إليها باسم “العرض”). يجب تقديم أي عرض مماثل لذلك فقط من خلال عرض ذي صلة أو وثائق أخرى تحدد شروطه وأحكامه المادية. لا يشكل أي محتوى وارد في هذه الوثيقة توصية أو طلبًا أو دعوة أو إغراء أو ترويجًا أو عرضًا لشراء أو بيع أي منتج استثماري من شركة “إيكويتيز فيرست” أو “إيكويتيز فيرست هولدينجز المحدودة” أو الشركات التابعة لها (يشار إليها مجتمعة باسم “إيكويتيز فيرست”)، ولا يجوز تفسير هذه الوثيقة بأي شكل من الأشكال على أنها مشورة استثمارية أو قانونية أو ضريبية أو توصية أو مرجع أو إقرار مقدم من شركة “إيكويتيز فيرست”. وعليك طلب المشورة المالية المستقلة قبل اتخاذ أي قرار استثماري بشأن منتج مالي معين.

تحتفظ هذه الوثيقة بحقوق الملكية الفكرية لشركة “إيكويتيز فيرست” في الولايات المتحدة ودول أخرى، ويشمل ذلك على سبيل المثال لا الحصر، الشعارات الخاصة بها وغيرها من العلامات التجارية وعلامات الخدمة المسجلة وغير المسجلة. تحتفظ الشركة بجميع الحقوق المتعلقة بملكيتها الفكرية الواردة في هذه الوثيقة. ينبغي لمستلمي هذه الوثيقة عدم توزيعها أو نشرها أو إعادة إنتاجها أو إتاحتها كليًّا أو جزئيًّا بأي شكل من الأشكال لأي شخص آخر، لا سيما الأشخاص في دولة قد يؤدي توزيع هذه الوثيقة فيها إلى خرق أي شرط قانوني أو تنظيمي.

لا تقدم شركة “إيكويتيز فيرست” أي تعهد أو ضمان فيما يتعلق بهذه الوثيقة، وتخلي مسؤوليتها صراحة عن أي ضمان ضمني بموجب القانون. وعليه تقر بأن شركة “إيكويتيز فيرست” ليست مسؤولة تحت أي ظرف من الظروف عن أي أضرار مباشرة أو غير مباشرة أو خاصة أو تبعية أو عرضية أو عقابية أيًّا كان نوعها، منها على سبيل المثال لا الحصر، أي أرباح مفقودة أو فرص ضائعة، حتى إذا تم إخطار الشركة بإمكانية وقوع مثل هذه الأضرار.

تدلي شركة “إيكويتيز فيرست” بالتصريحات الإضافية الآتية التي قد تطبق في دول الاختصاص القضائي المذكورة:

دبي: تخضع شركة “إيكويتيز فيرست هونج كونج المحدودة” (التي يشار إليها باسم “المكتب التمثيلي بمركز دبي المالي العالمي”) الكائنة في مبنى حي البوابة 4، الطابق 6، المكتب 7، مركز دبي المالي العالمي (التي تحمل ترخيصًا تجاريًّا رقم CL7354) للوائح سلطة دبي للخدمات المالية بصفتها مكتبًّا تمثيليًّا (رقم مرجع الشركة لدى سلطة دبي للخدمات المالية:F008752 ). جميع الحقوق محفوظة.

تُستخدم المواد الواردة في هذه الوثيقة لأغراض معلوماتية فقط وينبغي عدم تفسيرها على أنها مشورة مالية أو عرض أو طلب أو توصية لشراء منتجات مالية أو بيعها. تعد المعلومات الواردة في هذه الوثيقة عامة بطبيعتها، وأي مشورة واردة هنا هي عامة وقد تم إعدادها من دون النظر إلى أهدافك أو وضعك المالي أو ملاءمة منتجاتك المالية أو احتياجاتك. لذا قبل استخدام أي من هذه المعلومات، يجب أن تفكر في مدى ملاءمتها لأهدافك ووضعك المالي واحتياجاتك وطبيعة المنتج المالي ذي الصلة. يمكنك استشارة مستشار مالي معتمد إذا لم تكن بعض محتويات هذه الوثيقة واضحة بالنسبة إليك.

تختص هذه الوثيقة بمنتج مالي لا يخضع لأي شكل من أشكال التنظيم أو الاعتماد الخاص بسلطة دبي للخدمات المالية. لا تتحمل سلطة دبي للخدمات المالية أي مسؤولية عن مراجعة أي وثائق تتعلق بهذا المنتج المالي أو التحقق منها. وعليه، لم تعتمد سلطة دبي للخدمات المالية هذه الوثيقة أو أي وثائق أخرى مرتبطة بها ولم تتخذ أي خطوات للتحقق من المعلومات الواردة فيها، ولا تتحمل أي مسؤولية ناجمة عنها.

أستراليا: تحمل شركة “إيكويتيز فيرست هولدينجز (أستراليا) ذات المسؤولية المحدودة” (رقم الشركة في أستراليا: 399 644 142) ترخيصًا لمزاولة الخدمات المالية في أستراليا (رقم الترخيص: 387079). جميع الحقوق محفوظة.

توجه المعلومات الواردة في هذه الوثيقة للأشخاص في أستراليا فقط المصنفين بأنهم عملاء في قطاع التجارة بالجملة على النحو المحدد في القسم 761G من قانون الشركات لعام 2001. قد يُقيد توزيع المعلومات على الأشخاص الذين لا تنطبق عليهم هذه المعايير بموجب القانون، ويجب على الأشخاص الذين يمتلكونها طلب المشورة ومراعاة أي قيود تتعلق بها.

تستخدم المواد الواردة في هذه الوثيقة لأغراض معلوماتية فقط وينبغي عدم تفسيرها على أنها عرض أو طلب أو توصية لشراء منتجات مالية أو بيعها.

تُعد المعلومات الواردة في هذه الوثيقة عامة بطبيعتها وليست مشورة شخصية بشأن المنتجات المالية. أي مشورة واردة في الوثيقة هي عامة فقط وقد تم إعدادها من دون النظر إلى أهدافك أو وضعك المالي أو احتياجاتك. لذا قبل استخدام أي من هذه المعلومات، يجب أن تفكر في مدى ملاءمتها لأهدافك ووضعك المالي واحتياجاتك وطبيعة المنتج المالي ذي الصلة. عليك طلب المشورة المالية المستقلة وقراءة بيانات الإفصاح ذات الصلة أو وثائق العرض الأخرى قبل اتخاذ أي قرار استثماري بشأن منتج مالي معين.

التوقعات غير مضمونة، ولا ينبغي الاعتماد عليها بشكل مفرط. تعتمد هذه المعلومات على الآراء التي تتبناها شركة إكويتيز فيرست هولدينغز (أستراليا) ذات مسؤولية محدودة خاصة كما في تاريخ نشر هذا المحتوى

هونغ كونغ: تمتلك شركة “إيكويتيز فيرست هولدينجز هونج كونج المحدودة” ترخيصًا من النوع 1 من لجنة هونغ كونغ للأوراق المالية والعقود الآجلة، وهي مرخصة في هونغ كونغ بموجب قانون مقرضي الأموال (ترخيص مقرض الأموال رقم 2025/1493). لم تراجع لجنة هونغ كونغ للأوراق المالية والعقود الآجلة هذه الوثيقة. لا تمثل هذه الوثيقة عرضًا لبيع أوراق مالية أو طلبًا لشراء أي منتج تديره أو تقدمه شركة “إيكويتيز فيرست هولدينجز هونج كونج المحدودة”، لكنها موجهة للمستثمرين المحترفين لا للأفراد أو المؤسسات التي تكون هذه العروض أو الدعوات غير قانونية أو محظورة بالنسبة إليهم.

كوريا: توجه هذه الوثيقة فقط للمستهلكين الماليين المحترفين أو المستثمرين المحترفين أو المستثمرين المؤهلين الذين يتسلحون بالمعرفة ويتمتعون بالخبرة الكافية للدخول في معاملات تمويل الأوراق المالية، وهي غير مخصصة للأشخاص الذين لا يستوفون هذه المعايير وينبغي عدم استخدامهم إياها.