Are capital markets adequately factoring the impact of climate change to the value of securities? Many institutional investors do not think so.[1] And until markets rectify this anomaly, mispriced climate risks may present significant opportunities for savvy stock buyers.[2]

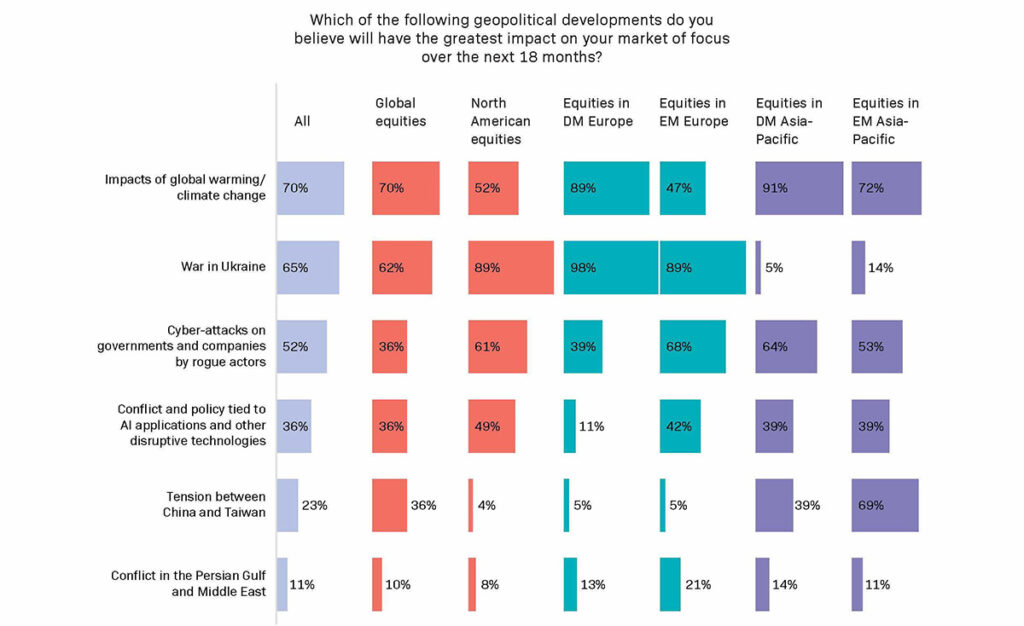

Investors believe climate change will be the most important geopolitical factor affecting equity prices over the next 18 months, according to a recent study based on the views of some 300 investment decision-makers from asset managers, foundations, pension schemes and endowments across the globe.

The timely report, produced by EquitiesFirst in collaboration with Institutional Investor’s Custom Research Lab, seeks to assess how persistent inflation, high interest rates, international conflict and pandemic recovery are influencing the near- and mid-term outlooks for global equity markets.

Asked what would have the greatest impact on stock markets over the next 18 months, 70% of respondents singled out climate change – ahead of war in Ukraine (65%) and cyber-attacks on governments and businesses (52%).

Varying climate concern

Investors’ views, however, diverged considerably depending on their regional equity remit. Those focused on developed markets in Europe and Asia Pacific were the most concerned about the impact of climate change.

By contrast, only around half of investors focused on North American equities saw climate change as a major risk, despite the increasingly destructive wildfires sweeping across the likes of California and Canada.

This lack of consensus around climate risk distorts equities valuations and may create an opportunity for equities investors to exploit.

Investors focused on North American markets might insufficiently discount stocks that would suffer most if a high carbon tax were imposed, or undervalue those that provide ways to reduce emissions.

That situation may be at least partly the result of US political pushback against investment that incorporates environmental, social and governance (ESG) factors. In fact, several of Wall Street’s largest financial institutions have warned that the backlash against ESG and, by extension, climate-related investment is now a material risk.[3]

In any case, most developed countries have pledged to reach net-zero emissions by 2050. To meet that target, there is still a very long way to go, so the chances are that more stringent climate regulations are coming. As a result, investors should consider the likely impact of current and expected climate policies on markets[4] – namely, which assets will suffer and which will benefit from such legislation.[5]

Reflecting on the opportunity

Investors focused on European developed-market stocks already seem to have nuanced views on the topic. Those interviewed for the study stressed that climate change and its impact were sources of both downside risk and upside opportunity because companies within their geographic purview were taking early and aggressive steps to transition to sustainable energy sources.

This not only makes companies in developed Europe more resilient to the imposition of more stringent climate regulation but could also give them a first-mover advantage as suppliers of products and services catering to an increasingly environmentally conscious global economy.

Meanwhile, the fact that investors focused on developed Asia showed a high level of climate concern – despite the region facing less stringent climate regulation and carbon pricing regimes than Europe – suggests equity valuations in those markets may already adequately reflect climate risks, including the likelihood that more onerous rules are on the way.

The concerns over climate risks in Asia’s developed markets are perhaps understandable, given that the impact of global warming on emerging Asia is likely to be more acute than in many other regions.

The investment opportunity offered by climate change is also particularly evident there. China dominates the solar panel supply chain globally and produces wind turbines at less than half the average cost internationally.[6] What’s more, the country continues to extend its lead in domestic renewable energy capacity, fuelling strong and steady growth in the sector.

Indonesia, meanwhile, exports vast quantities of nickel, cobalt and copper, largely for making electric vehicle batteries.

In fact, the worldwide push towards net-zero emissions will likely create opportunities in sectors and regions that investors may not yet even envisage.

Those wishing to get a piece of that action – whether for ethical reasons or monetary gain, or both – could consider tapping securities-backed financing. At a time of scarce liquidity, it can offer a more attractive way to raise capital for buying potentially undervalued stocks and diversifying portfolios without having to reduce exposure to other sectors and themes.

It may make sense to at least dip a toe into climate-related investment, as this is a theme that will continue to impact equity markets for a long time to come.

أعدت هذه الوثيقة خصيصاً للمستثمرين المعتمدين أو المستثمرين المتطورين ماليًّا أو المستثمرين المحترفين أو المستثمرين المؤهلين، على النحو الذي يقتضيه القانون أو غيره، وهي ليست موجهة للأشخاص الذين لا يستوفون المتطلبات ذات الصلة وينبغي عدم استخدامها من أجلهم. يستخدم محتوى هذه الوثيقة لأغراض إعلامية فقط ويغلب عليه الطابع العام ولا يلبي أي غاية محددة أو حاجة مالية معينة. تخص وجهات النظر والآراء الواردة في هذه الوثيقة أطرافًا ثالثة ولا تعكس بالضرورة وجهات نظر شركة “إيكويتيز فيرست” أو آراءها. لم تفحص شركة “إيكويتيز فيرست” المعلومات الواردة في هذه الوثيقة أو لم تتحقق منها بشكل مستقل، ولا تقدم أي تعهد بمدى دقتها أو اكتمالها. تخضع الآراء والمعلومات الواردة في هذه الوثيقة للتغيير من دون إشعار. لا يمثل محتوى الوثيقة عرضًا لبيع (أو طلب عرض شراء) أي أوراق مالية أو استثمارات أو منتجات مالية (يشار إليها باسم “العرض”). يجب تقديم أي عرض مماثل لذلك فقط من خلال عرض ذي صلة أو وثائق أخرى تحدد شروطه وأحكامه المادية. لا يشكل أي محتوى وارد في هذه الوثيقة توصية أو طلبًا أو دعوة أو إغراء أو ترويجًا أو عرضًا لشراء أو بيع أي منتج استثماري من شركة “إيكويتيز فيرست” أو “إيكويتيز فيرست هولدينجز المحدودة” أو الشركات التابعة لها (يشار إليها مجتمعة باسم “إيكويتيز فيرست”)، ولا يجوز تفسير هذه الوثيقة بأي شكل من الأشكال على أنها مشورة استثمارية أو قانونية أو ضريبية أو توصية أو مرجع أو إقرار مقدم من شركة “إيكويتيز فيرست”. وعليك طلب المشورة المالية المستقلة قبل اتخاذ أي قرار استثماري بشأن منتج مالي معين.

تحتفظ هذه الوثيقة بحقوق الملكية الفكرية لشركة “إيكويتيز فيرست” في الولايات المتحدة ودول أخرى، ويشمل ذلك على سبيل المثال لا الحصر، الشعارات الخاصة بها وغيرها من العلامات التجارية وعلامات الخدمة المسجلة وغير المسجلة. تحتفظ الشركة بجميع الحقوق المتعلقة بملكيتها الفكرية الواردة في هذه الوثيقة. ينبغي لمستلمي هذه الوثيقة عدم توزيعها أو نشرها أو إعادة إنتاجها أو إتاحتها كليًّا أو جزئيًّا بأي شكل من الأشكال لأي شخص آخر، لا سيما الأشخاص في دولة قد يؤدي توزيع هذه الوثيقة فيها إلى خرق أي شرط قانوني أو تنظيمي.

لا تقدم شركة “إيكويتيز فيرست” أي تعهد أو ضمان فيما يتعلق بهذه الوثيقة، وتخلي مسؤوليتها صراحة عن أي ضمان ضمني بموجب القانون. وعليه تقر بأن شركة “إيكويتيز فيرست” ليست مسؤولة تحت أي ظرف من الظروف عن أي أضرار مباشرة أو غير مباشرة أو خاصة أو تبعية أو عرضية أو عقابية أيًّا كان نوعها، منها على سبيل المثال لا الحصر، أي أرباح مفقودة أو فرص ضائعة، حتى إذا تم إخطار الشركة بإمكانية وقوع مثل هذه الأضرار.

تدلي شركة “إيكويتيز فيرست” بالتصريحات الإضافية الآتية التي قد تطبق في دول الاختصاص القضائي المذكورة:

دبي: تخضع شركة “إيكويتيز فيرست هونج كونج المحدودة” (التي يشار إليها باسم “المكتب التمثيلي بمركز دبي المالي العالمي”) الكائنة في مبنى حي البوابة 4، الطابق 6، المكتب 7، مركز دبي المالي العالمي (التي تحمل ترخيصًا تجاريًّا رقم CL7354) للوائح سلطة دبي للخدمات المالية بصفتها مكتبًّا تمثيليًّا (رقم مرجع الشركة لدى سلطة دبي للخدمات المالية:F008752 ). جميع الحقوق محفوظة.

تُستخدم المواد الواردة في هذه الوثيقة لأغراض معلوماتية فقط وينبغي عدم تفسيرها على أنها مشورة مالية أو عرض أو طلب أو توصية لشراء منتجات مالية أو بيعها. تعد المعلومات الواردة في هذه الوثيقة عامة بطبيعتها، وأي مشورة واردة هنا هي عامة وقد تم إعدادها من دون النظر إلى أهدافك أو وضعك المالي أو ملاءمة منتجاتك المالية أو احتياجاتك. لذا قبل استخدام أي من هذه المعلومات، يجب أن تفكر في مدى ملاءمتها لأهدافك ووضعك المالي واحتياجاتك وطبيعة المنتج المالي ذي الصلة. يمكنك استشارة مستشار مالي معتمد إذا لم تكن بعض محتويات هذه الوثيقة واضحة بالنسبة إليك.

تختص هذه الوثيقة بمنتج مالي لا يخضع لأي شكل من أشكال التنظيم أو الاعتماد الخاص بسلطة دبي للخدمات المالية. لا تتحمل سلطة دبي للخدمات المالية أي مسؤولية عن مراجعة أي وثائق تتعلق بهذا المنتج المالي أو التحقق منها. وعليه، لم تعتمد سلطة دبي للخدمات المالية هذه الوثيقة أو أي وثائق أخرى مرتبطة بها ولم تتخذ أي خطوات للتحقق من المعلومات الواردة فيها، ولا تتحمل أي مسؤولية ناجمة عنها.

أستراليا: تحمل شركة “إيكويتيز فيرست هولدينجز (أستراليا) ذات المسؤولية المحدودة” (رقم الشركة في أستراليا: 399 644 142) ترخيصًا لمزاولة الخدمات المالية في أستراليا (رقم الترخيص: 387079). جميع الحقوق محفوظة.

توجه المعلومات الواردة في هذه الوثيقة للأشخاص في أستراليا فقط المصنفين بأنهم عملاء في قطاع التجارة بالجملة على النحو المحدد في القسم 761G من قانون الشركات لعام 2001. قد يُقيد توزيع المعلومات على الأشخاص الذين لا تنطبق عليهم هذه المعايير بموجب القانون، ويجب على الأشخاص الذين يمتلكونها طلب المشورة ومراعاة أي قيود تتعلق بها.

تستخدم المواد الواردة في هذه الوثيقة لأغراض معلوماتية فقط وينبغي عدم تفسيرها على أنها عرض أو طلب أو توصية لشراء منتجات مالية أو بيعها.

تُعد المعلومات الواردة في هذه الوثيقة عامة بطبيعتها وليست مشورة شخصية بشأن المنتجات المالية. أي مشورة واردة في الوثيقة هي عامة فقط وقد تم إعدادها من دون النظر إلى أهدافك أو وضعك المالي أو احتياجاتك. لذا قبل استخدام أي من هذه المعلومات، يجب أن تفكر في مدى ملاءمتها لأهدافك ووضعك المالي واحتياجاتك وطبيعة المنتج المالي ذي الصلة. عليك طلب المشورة المالية المستقلة وقراءة بيانات الإفصاح ذات الصلة أو وثائق العرض الأخرى قبل اتخاذ أي قرار استثماري بشأن منتج مالي معين.

التوقعات غير مضمونة، ولا ينبغي الاعتماد عليها بشكل مفرط. تعتمد هذه المعلومات على الآراء التي تتبناها شركة إكويتيز فيرست هولدينغز (أستراليا) ذات مسؤولية محدودة خاصة كما في تاريخ نشر هذا المحتوى

هونغ كونغ: تمتلك شركة “إيكويتيز فيرست هولدينجز هونج كونج المحدودة” ترخيصًا من النوع 1 من لجنة هونغ كونغ للأوراق المالية والعقود الآجلة، وهي مرخصة في هونغ كونغ بموجب قانون مقرضي الأموال (ترخيص مقرض الأموال رقم 2025/1493). لم تراجع لجنة هونغ كونغ للأوراق المالية والعقود الآجلة هذه الوثيقة. لا تمثل هذه الوثيقة عرضًا لبيع أوراق مالية أو طلبًا لشراء أي منتج تديره أو تقدمه شركة “إيكويتيز فيرست هولدينجز هونج كونج المحدودة”، لكنها موجهة للمستثمرين المحترفين لا للأفراد أو المؤسسات التي تكون هذه العروض أو الدعوات غير قانونية أو محظورة بالنسبة إليهم.

كوريا: توجه هذه الوثيقة فقط للمستهلكين الماليين المحترفين أو المستثمرين المحترفين أو المستثمرين المؤهلين الذين يتسلحون بالمعرفة ويتمتعون بالخبرة الكافية للدخول في معاملات تمويل الأوراق المالية، وهي غير مخصصة للأشخاص الذين لا يستوفون هذه المعايير وينبغي عدم استخدامهم إياها.