Are capital markets adequately factoring the impact of climate change to the value of securities? Many institutional investors do not think so.[1] And until markets rectify this anomaly, mispriced climate risks may present significant opportunities for savvy stock buyers.[2]

Investors believe climate change will be the most important geopolitical factor affecting equity prices over the next 18 months, according to a recent study based on the views of some 300 investment decision-makers from asset managers, foundations, pension schemes and endowments across the globe.

The timely report, produced by EquitiesFirst in collaboration with Institutional Investor’s Custom Research Lab, seeks to assess how persistent inflation, high interest rates, international conflict and pandemic recovery are influencing the near- and mid-term outlooks for global equity markets.

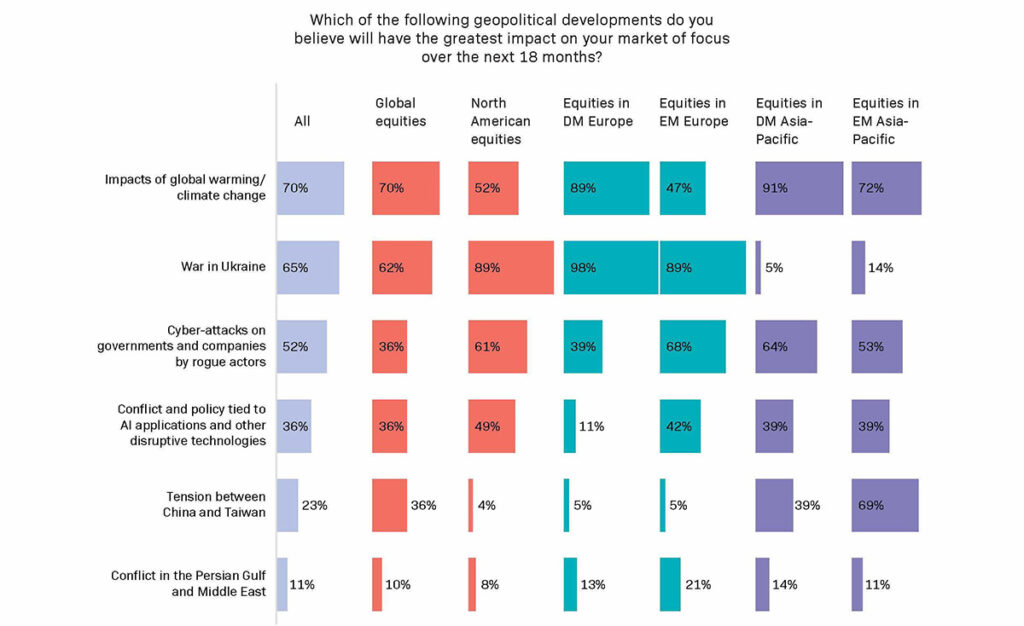

Asked what would have the greatest impact on stock markets over the next 18 months, 70% of respondents singled out climate change – ahead of war in Ukraine (65%) and cyber-attacks on governments and businesses (52%).

Varying climate concern

Investors’ views, however, diverged considerably depending on their regional equity remit. Those focused on developed markets in Europe and Asia Pacific were the most concerned about the impact of climate change.

By contrast, only around half of investors focused on North American equities saw climate change as a major risk, despite the increasingly destructive wildfires sweeping across the likes of California and Canada.

This lack of consensus around climate risk distorts equities valuations and may create an opportunity for equities investors to exploit.

Investors focused on North American markets might insufficiently discount stocks that would suffer most if a high carbon tax were imposed, or undervalue those that provide ways to reduce emissions.

That situation may be at least partly the result of US political pushback against investment that incorporates environmental, social and governance (ESG) factors. In fact, several of Wall Street’s largest financial institutions have warned that the backlash against ESG and, by extension, climate-related investment is now a material risk.[3]

In any case, most developed countries have pledged to reach net-zero emissions by 2050. To meet that target, there is still a very long way to go, so the chances are that more stringent climate regulations are coming. As a result, investors should consider the likely impact of current and expected climate policies on markets[4] – namely, which assets will suffer and which will benefit from such legislation.[5]

Reflecting on the opportunity

Investors focused on European developed-market stocks already seem to have nuanced views on the topic. Those interviewed for the study stressed that climate change and its impact were sources of both downside risk and upside opportunity because companies within their geographic purview were taking early and aggressive steps to transition to sustainable energy sources.

This not only makes companies in developed Europe more resilient to the imposition of more stringent climate regulation but could also give them a first-mover advantage as suppliers of products and services catering to an increasingly environmentally conscious global economy.

Meanwhile, the fact that investors focused on developed Asia showed a high level of climate concern – despite the region facing less stringent climate regulation and carbon pricing regimes than Europe – suggests equity valuations in those markets may already adequately reflect climate risks, including the likelihood that more onerous rules are on the way.

The concerns over climate risks in Asia’s developed markets are perhaps understandable, given that the impact of global warming on emerging Asia is likely to be more acute than in many other regions.

The investment opportunity offered by climate change is also particularly evident there. China dominates the solar panel supply chain globally and produces wind turbines at less than half the average cost internationally.[6] What’s more, the country continues to extend its lead in domestic renewable energy capacity, fuelling strong and steady growth in the sector.

Indonesia, meanwhile, exports vast quantities of nickel, cobalt and copper, largely for making electric vehicle batteries.

In fact, the worldwide push towards net-zero emissions will likely create opportunities in sectors and regions that investors may not yet even envisage.

Those wishing to get a piece of that action – whether for ethical reasons or monetary gain, or both – could consider tapping securities-backed financing. At a time of scarce liquidity, it can offer a more attractive way to raise capital for buying potentially undervalued stocks and diversifying portfolios without having to reduce exposure to other sectors and themes.

It may make sense to at least dip a toe into climate-related investment, as this is a theme that will continue to impact equity markets for a long time to come.

Past performance does not guarantee future returns, and individual returns are not guaranteed or warranted.

This Document is intended solely for accredited investors, sophisticated investors, professional investors, or otherwise qualified investors, as may be required by law or otherwise, and it is not intended for, and should not be used by, persons who do not meet the relevant requirements. The content provided herein is for informational purposes only and is general in nature and not targeted to any specific objective or financial need. The views and opinions expressed in this Document have been prepared by third parties and do not necessarily reflect the views and opinions of EquitiesFirst. EquitiesFirst has not independently examined or verified the information provided herein, and no representation is made that it is accurate or complete. Opinions and information herein are subject to change without notice. The content provided does not constitute an offer to sell (or solicitation of an offer to purchase) any securities, investments, or any financial products (“Offer”). Any such Offer shall only be made through a relevant offering or other documentation which sets forth its material terms and conditions. Nothing contained in this Document shall constitute a recommendation, solicitation, invitation, inducement, promotion, or offer for the purchase or sale of any investment product by Equities First Holdings, LLC or its subsidiaries (collectively, “EquitiesFirst”), nor shall this Document be construed in any way as investment, legal, or tax advice, or as a recommendation, reference, or endorsement by EquitiesFirst. You should seek independent financial advice prior to making an investment decision about a financial product.

This Document contains the intellectual property of EquitiesFirst in the United States and other countries, including, without limitation, their respective logos and other registered and unregistered trademarks and service marks. EquitiesFirst reserves all rights in and to their intellectual property contained in this Document. The Document should not be distributed, published, reproduced or otherwise made available in whole or in part by recipients to any other person and, in particular, should not be distributed to persons in any country where such distribution may lead to a breach of any legal or regulatory requirement.

EquitiesFirst make no representation or warranty with respect to this Document and expressly disclaim any implied warranty under law. You acknowledge that EquitiesFirst is not liable under any circumstances for any direct, indirect, special, consequential, incidental, or punitive damages whatsoever, including, without limitation, any lost profits or lost opportunity, even if EquitiesFirst has been advised of the possibility of such damages.

EquitiesFirst makes the following further statements that may be applicable in the stated jurisdiction:

Australia: Equities First Holdings (Australia) Pty Ltd (ACN: 142 644 399) holds an Australian Financial Services Licence (AFSL Number: 387079). All rights reserved.

The information contained on this Document is intended for persons located in Australia only and classified as a Wholesale Client only as defined in Section 761G of the Corporations Act 2001. The distribution of information to persons outside this criteria may be restricted by law and persons who come into possession of it should seek advice and observe any such restriction.

The material contained in this Document is for information purposes only and should not be construed as an offer or solicitation or recommendation to buy or sell financial products.

The information contained in this Document is intended to be general in nature and is not personal financial product advice. Any advice contained in the Document is general advice only and has been prepared without considering your objectives, financial situation or needs. Before acting on any information, you should consider the appropriateness of the information provided and the nature of the relevant financial product having regard to your objectives, financial situation and needs. You should seek independent financial advice and read the relevant disclosure statements or other offer documents prior to making an investment decision about a financial product.

Forecasts are not guaranteed, and undue reliance should not be placed on them. This information is based on views held by Equities First Holdings (Australia) Pty Ltd as at the publishing date of this material.

Dubai: Equities First Holdings Hong Kong Ltd (DIFC Representative Office) at Gate Precinct Building 4, 6th Floor, Office 7, Dubai International Financial Centre (commercial license number CL7354) is regulated by the Dubai Financial Services Authority (“DFSA”) as a Representative Office (DFSA Firm Reference No.: F008752). All rights reserved.

The material contained in this document is for information purposes only and should not be construed as financial advice, including an offer or solicitation or recommendation to buy or sell financial products. The information contained in this document is intended to be general in nature and any advice contained in this document is general advice only and has been prepared without considering your objectives, financial situation, suitability of the financial products or your needs. Before acting on any information, you should consider the appropriateness of the information provided and the nature of the relevant financial product having regard to your objectives, financial situation and needs. If you do not understand the contents of this document, you should consult an authorised financial adviser.

This document relates to a financial product which is not subject to any form of regulation or approval by the DFSA. The DFSA has no responsibility for reviewing or verifying any documents in connection with this financial product. Accordingly, the DFSA has not approved this document or any other associated documents nor taken any steps to verify the information set out in this document, and has no responsibility for it.

Hong Kong: Equities First Holdings Hong Kong Limited is licensed under the Money Lenders Ordinance (Money Lender’s Licence No. 1493/2025) and to carry on the business of dealing in securities (Type 1 licence) under the Securities and Futures Ordinance (“SFO”) (CE No. BFJ407). This Document has not been reviewed by the Hong Kong Securities and Futures Commission. It is not intended as an offer to sell securities or a solicitation to buy any product managed or provided by Equities First Holdings Hong Kong Limited and is only intended for persons who qualify as Professional Investors under the SFO. This document is not directed to individuals or organizations for whom such offers or invitations would be unlawful or prohibited.

Korea: The foregoing is intended solely for sophisticated investors, professional investors or otherwise qualified investors who have sufficient knowledge and experience in entering into securities financing transactions. It is not intended for, and should not be used by, persons who do not meet those criteria.

United Kingdom: Equities First (London) Limited is authorised and regulated in the UK by the Financial Conduct Authority (“FCA”). In the UK, this Document is only being distributed and made available to persons of the kind described in Article 19(5) (investment professionals) and Article 49(2) (high net worth companies, unincorporated associations etc.) of Part IV of the Financial Services and Markets Act 2000 (Financial Promotion) Order 2005 (‘’FPO’’) and any investment activity to which this presentation relates is only available to, and will only be engaged in with, such persons. Persons who do not have professional experience in matters relating to investment or who are not persons to whom Article 49 of the FPO applies should not rely on this document. This Document is only prepared for and available to persons who qualify as Professional Investors under the Markets in Financial Instruments Directive.